Let’s say you have just turned 50, or you are already in early 50’s, and you plan to retire in about 10 years. It’s probably the high time to work out a plan and put it into practice. Thinking of retirement, the very first question that comes to mind is how much savings would be enough that could last comfortably for 30-40 years. The second question would be what will be my/our expenses in retirement. Both of these questions are inter-dependent and often are the most intriguing questions facing most people who are not yet retired but plan to retire not too distant in the future.

On the other hand, if you are still in your 40s, you may think it is too early to ask these questions. However, it never hurts to run some numbers and plan accordingly. Moreover, if you plan early, you will have more choices and time to adjust your plan.

Obviously, these questions are not very straightforward to answer. There are many variables that can differ from one person to another. The first question that you need to tackle is how much spending/expenses a year you will have in retirement. The answer to the other question with regard to the amount of savings will largely depend on our ability to answer the first question fairly accurately. In this article, we will try to address these questions and try to develop some estimates. We will also try to demonstrate how a modest level of savings can be grown to significant sums that can last for a long time.

We can use a hypothetical couple – John and Lisa – let’s assume they both are 50 years of age and want to retire in 10 years at 60 years of age. Their current savings are modest at $ 300,000 and mostly in 401K, and/or IRAs. Their current household gross income is $ 125,000 a year. They recognize that they need to do some serious planning and make some tough choices if they hope to have a comfortable retirement starting 10 years.

John and Lisa currently carry a mortgage on their house and have one child in college whom they are supporting. First, they make some bold decisions. They decide that they will make some extra payments each year on the mortgage and will be able to pay off the house by the time they retire. They decide that they will not carry any car loans or credit card debt into retirement. They also decide that they both will increase their current 401K contributions to 16% of their earnings until they retire. This will help boost their savings significantly.

Estimation of Expenses in Retirement:

Next task is to figure out how much their spending/expenses will be when they retire in 10 years. There are basically two ways to calculate spending. First one is to simply make a list and add the likely expenses in retirement; however, one is likely to underestimate or overestimate some expenses. The second method that we feel is more appropriate is to take the current income and subtract all the expenses that you will not incur in retirement. Also, add any expenses that you may have in retirement that you do not have currently; for example, there may be an increase in medical premiums/costs. Then, adjust this remaining amount for inflation for the number of years that are left prior to retirement. It basically means to figure out how much of the money currently goes into items that will no longer be needed. This method will ensure your current lifestyle into retirement years.

This is what they come up with:

- They will not need to put the 16% savings contributions into their 401K or retirement funds any longer.

- Their tax bracket would be much lower, so will need to account for that reduction.

- They will not be putting any more money into Social Security/Medicare deductions, as they would not have any earned income.

- Besides they will not have work-related expenses, like commuting, new clothing, dry-cleaning expenses, etc.

- They should be done with kid’s college education which will cut down another $ 14,000 a year.

- They will not have the house mortgage payments anymore (monthly mortgage $ 1,200 or $ 14,400 yearly).

- They will not have the current medical premiums that get deducted from their paychecks, but instead, they will need to earmark higher medical premiums since they will not be eligible for Medicare until 65.

|

Total current gross earnings Minus (-) Current 401/IRA contributions Social security/Medicare deductions Taxes (federal and State) Medical premium deductions Any work-related expenses Kid’s college expenses Home Mortgage payments Plus (+) Extra costs or premium for Medical Insurance. |

John and Lisa use a Google spreadsheet (prepared by Financially Free Investor, available here) to run the numbers and come to a conclusion that nearly 60% of their current income goes to expense-items that they will no longer have or need in retirement. That means they would only require 40% of their current income to support their existing lifestyle. Based on their current gross income of $ 125,000, it comes to $ 50,000 a year in today’s prices. However, due to inflation in the next 10 years (assuming at 2.5% a year), they will require $ 64,000 a year. In addition, they plan to earmark another $ 1,000 a month or $ 12,000 a year for medical premiums/costs. So, they figure out that they will need roughly $ 76,000 a year to be able to sustain their current living standards. They round it off to $ 75,000 a year.

|

40% of the current Income: Inflation adjusted Amount (10 years later): Plus Medical Premiums in retirement: |

$ 50,000 $ 64,000 $ 12,000 |

|

Total: |

$ 76,000 a year (~=75,000 a year). |

How Much Savings Are Needed?

John and Lisa decide that John would start taking his social security benefits at the earliest eligibility age of 62 years, but delay Lisa’s social security until she gets to 70 years of age. By doing this, they will be able to balance out the income needs along with compounding Lisa’s social security benefits to the highest payout possible.

John and Lisa also assume that they will withdraw up to 6% income from their investment capital at the time of retirement at age 60 until they get to the age 70. This is when they start withdrawing the second social security benefits. Now some folks will argue that 6% income is too high to withdraw. However, even if we think it is too high, in the worst case scenario, their portfolio may not grow as much they would like during their age from 60-70 years. After 70 years, when they have the second social security coming in, their withdrawal percentage will get reduced significantly.

By reverse calculation, this couple will require $ 1.25 million (75,000/0.06) in investment savings at the time of retirement. They only have $ 300,000 today. Without any more contributions, to grow this amount to 1.25 million in 10 years will require compounding this amount at a rate of 16% per annum, which is almost unachievable. But the good thing is that they are still working. They have already decided to increase their 401K pre-tax contributions to 16% of their income, and along with the employer’s matching, they will likely be able to achieve the target. Any further rise in their income would also be put away to ROTH IRA accounts.

Investment Returns Simulations:

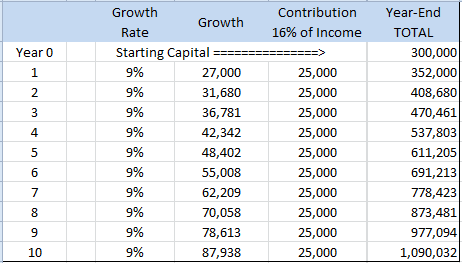

John and Lisa get to the task of planning how they could get to the target of $ 1.25 million in 10 years. In the first example, they assume that their investments would grow at a very steady rate of 9% a year for the next 10 years, while they contributed 16% of income every year along with 4% from employer’s matching.

Table-1

With 9% steady growth rate, they are very close to their target of $ 1.25 million, but not entirely. Further, the above assumption of 9% growth every year would probably be fine over 2 or 3 decades, but over 10 years it may not be very realistic. The market’s ups and downs from year to year can change the outcome. If the history is any guide, it can vary greatly depending on how the markets do in the next 10 years. Let’s run some numbers for John and Lisa, from the past for historical perspective to see what is realistic.

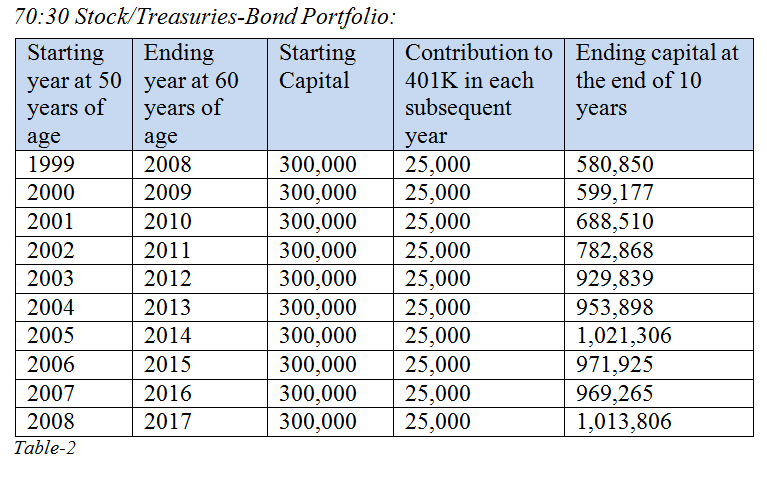

We will consider every 10-year period, starting from the year 1999; for example, 10-year periods such as 1999-2008, 2000-2009, 2001-2010 and so on. We will assume that they invested rather conservatively with a mix of 70% in stocks, and 30% in Treasuries and bonds. Let’s see how they would have fared in each scenario.

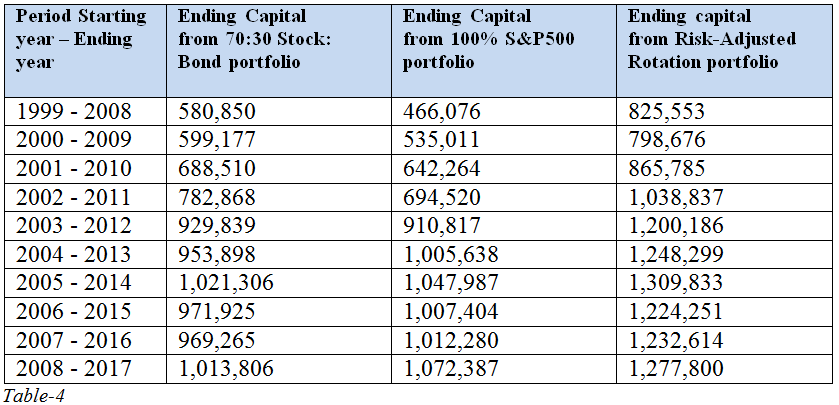

Now, what if, John and Lisa had decided to invest everything in S&P 500. Let’s see how they would have fared in this scenario:

As you can see if they had started their 10-year plan anytime between years 1999 and 2002, they would be much behind their intended target. The 10-year periods of 1999-2008, 2000-2009 and 2001-2010 were most undesirable as they had to bear two full-blown recessions/corrections and did not have enough time to recover from 2008 debacle. It is clear if John and Lisa had started the plan anytime between 1999 and 2002, there was no way they could have retired at the end of 10 years with the level of spending expenses as they had planned. The only options would have been either to postpone the retirement for a few years until the markets recovered or to cut down on their lifestyle significantly.

Now, for the sake of comparison, let’s also run the numbers if John and Lisa had decided to invest in a Conservative Risk-Adjusted Rotation portfolio (based on back-tested numbers). This portfolio rotates between S&P 500 fund and the treasury/bond funds. When the market is relatively strong, the more funds are invested in the market; however, when the market starts declining or enters into a correction phase, more funds get switched to treasuries and bonds. Such a portfolio would generally underperform slightly during strong bull markets, but protect the capital during major corrections or recessions.

Author’s Note: The above Risk-Adjusted Rotation portfolio is part of FFI’s Marketplace service “High Income DIY Portfolios.”

Comparison of 3 Investment portfolios:

Initial Capital = $ 300,000

Additional Contribution= $ 25,000 each year for 10 years

However, for the sake of simplicity, let’s assume, John and Lisa would get a constant return of 8% over 10 years, which is not overly optimistic. With this rate of growth, their savings and contributions over 10 years will accumulate to 1.01 million. Let’s round it off to $ 1.0 million. As we can see, John and Lisa would fall short of their target of $ 1.25 million. However, the gap is not huge and can be managed with some innovative thinking. The other solution may be that one or both of them work some part-time job for a couple more years; however, not a desirable outcome. Let’s look at some alternatives to manage the gap.

Bridging The Gap:

For John and Lisa, the other solution may be as follows:

- They reserve 2 years of expenses in cash from the total capital, a total of $ 150,000 @ $ 75,000 per year, leaving the investment capital to $ 850,000.

- Also, they had already decided that John will start withdrawing social-security at the earlier eligible age of 62. Due to early withdrawal, he will get 75-80% of the full benefits. We will assume that SS-1 to be $ 1,500 a month and grow at a very conservative rate of 1% per annum due to COLA (Cost Of Living Adjustments).

- This will allow Lisa to wait until the age of 70 years to collect and let the social-security benefits be compounded to a much higher amount. We will assume that the SS-2 will be $ 3,000 per month, starting at 70 years and grow at 1% per annum by COLA adjustments.

- However, at age 70, due to inflation (from age 60-70 years), their expenses would go up as well, and they would need roughly $ 94,000 to keep the same purchasing power as of $ 75,000 (when they were 60).

- They assume that investments of $ 850,000 ($ 1.0 million – 150K reserve) will grow at a conservative rate of @8%.

COLA – Cost Of Living Adjustment – (Source: Investopedia)

An adjustment made to Social Security and Supplemental Security Income to counteract the effects of inflation. Cost-of-living adjustments (COLAs) are generally equal to the percentage increase in the consumer price index for urban wage earners and clerical workers (CPI-W) for a specific period.

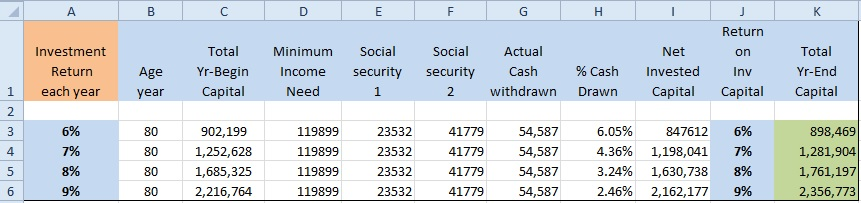

Below is the table that simulates the income and withdrawals from the age of 60-80 years.

Explanation and assumptions:

- Column A shows the age in years.

- Column B shows the starting capital at the beginning of the year.

- Column C shows the needed income each year. For the first two years, they need a fixed amount of $ 75,000 each year. After that, we will add 2.5% each year for inflation.

- Column D shows the social security payments for John, the first earner, assuming he starts withdrawing at 62 years of age (the earliest eligible date). We will assume that social security payment increases at an average rate of 1.0% (Cola adjustment).

- Column E shows the social security payments for Lisa, the second earner, assuming she starts withdrawing at 70 years of age (the late withdrawal date), so as to get higher payments. We will assume that she gets $ 3,000 per month starting at age 7 years. Also, social security payment increases at an average rate of 1.0% (Cola adjustment) after that.

- Column F is the actual cash withdrawn from the invested capital. Column F = Column C – Column D – Column E

- Column G shows the percentage of cash withdrawn. Column G = Column F / Column B

- Column H is the net investible amount after taking out the needed income.

- Column I: Rate of return on the invested capital = 8% per annum.

- Column K is the total balance amount at the end of each year, after accounting for withdrawals and the growth of the capital.

Table-5

Now, there is no guarantee that the future returns will be at 8%. It can be less or more. It may depend on their investment choices and market conditions. Let’s see, what their net balance would be at the age of 80, assuming different rates of return, everything else being the same. In the below table, we are only showing the last line only (at age 80) from table-5, assuming different rates of return.

Table-6

As you see, a lot depends on what the average rate of return is from the investments. If they get only 6% rate of return, they are not doing so good, as their capital is reducing, albeit slowly. If that were to occur, they should modify their lifestyle and reduce spending by about 10%. However, if they were to get an average rate of 8%, which is highly feasible, they have nothing to worry as their net balance at 80 years would be 70% higher than when they started, in addition to the consistent income withdrawn. Anything more than 8% would, of course, be icing on the cake.

Conclusion:

The simple conclusion is that if you are already 50 years old or more and have not planned for a possible retirement, it is high time that you should do it. Of course, it can always be done prior to getting to 50, but your numbers may have a little higher margin of error. It is always prudent to start saving from an early age, but as John and Lisa’s example shows, it is never too late. Even if you have modest savings by the time you turn 50, there is still ample time to make a plan, ramp up the savings/contributions to retirement accounts and compound the savings. However, more you delay it, harder will be the choices.

Author’s note: If you like this article, please click on the “Follow” button at the top of the article. In our SA Marketplace service “High Income DIY Portfolios,” we provide two high-income portfolios, one conservative portfolio, and another hi-growth portfolio. For more details, please click on the image just below our logo at the top of the article. We are currently running the 2-week free trial and discounted pricing.

Full Disclaimer: The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Please always do further research and do your own due diligence before making any investments. Every effort has been made to present the data/information accurately; however, the author does not claim 100% accuracy. Any stock portfolio or strategy presented here is only for demonstration purposes.

Additional Disclosure: I am/we are long ABT, ABBV, JNJ, PFE, NVS, NVO, CL, CLX, GIS, UL, NSRGY, PG, MON, ADM, MO, PM, KO, DEO, MCD, WMT, WBA, CVS, LOW, CSCO, MSFT, INTC, T, VZ, VTR, CVX, XOM, VLO, HCP, O, OHI, NNN, STAG, WPC, MAIN, NLY, PCI, PDI, PFF, RFI, RNP, UTF, EVT, FFC, KYN, NMZ, NBB, HQH, JPC, JRI, TLT.MCD, WMT, WBA, CVS, LOW, CSCO, MSFT, INTC, T, VZ, VTR, CVX, XOM, VLO, HCP, O, OHI, NNN, STAG, WPC, MAIN, NLY, PCI, PDI, PFF, RFI, RNP, UTF, EVT, FFC, KYN, NMZ, NBB, HQH, JPS, JRI, TLT.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Tech