In a Forbes article last year, I explained that “over the past three decades, corporations have been increasingly executing sale/leaseback transactions – usually to better allocate capital, but also in many cases to manage residual real estate risk.”

Remember that in a sale/leaseback transaction, the owner-occupant of a commercial property sells the asset it owns and occupies by executing a long-term lease with a real estate investor. This structured financing alternative has evolved into an attractive strategy for many corporations to unlock the value of their real estate assets.

Many corporations earn a higher return on their core business as compared to investing their capital in owned real estate. This off-balance sheet alternative provides the occupier 100% of the value of the property compared to traditional mortgage financing, which is usually around 65% loan-to-value.

In the same Forbes article, I explained that “the spigot of capital flowing into corporate machinery and equipment will serve as a catalyst for the Net Lease REIT consolidators that have the strongest management teams and lowest weighted average cost of capital.”

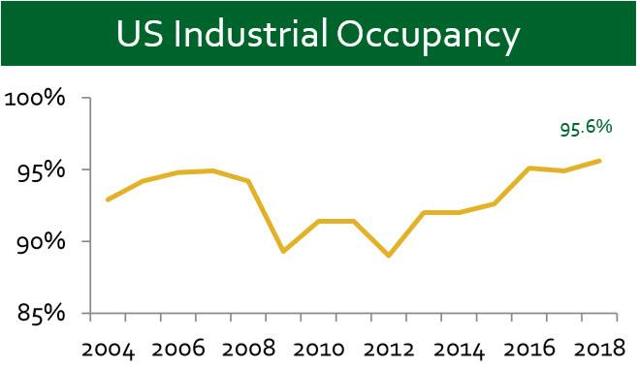

Current economic indicators are very favorable for the U.S. industrial real estate sector due to (1) rising GDP, (2) rampant e-commerce growth, (3) limited new construction since 2010, and (4) manufacturing growth.

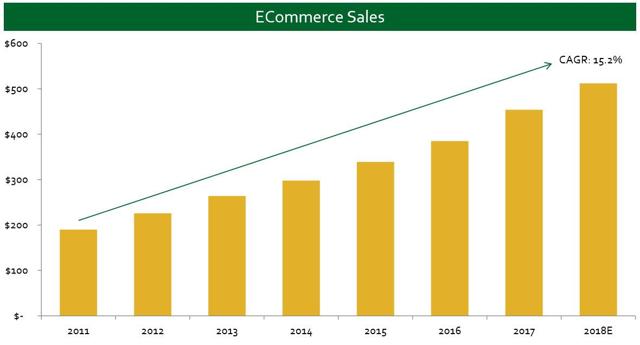

The entire retail industry has been shifting its focus from traditional brick-and-mortar stores to e-commerce platforms which has led to significant demand for large, modern industrial distribution centers. In the U.S., e-commerce sales are expected to increase to over $500 billion in 2018. Excluding food, fuel, and auto, e-commerce represents approximately 16% of total U.S. retail sales.

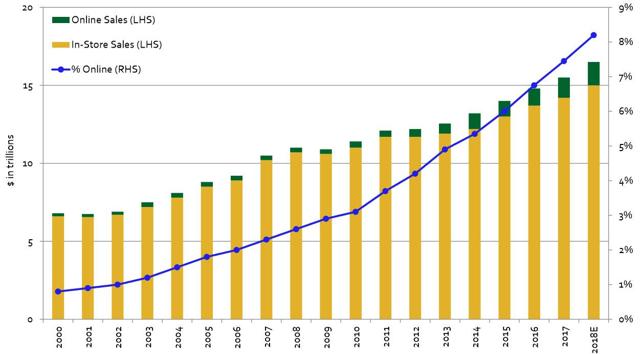

Global consumer habits continue to change resulting in ever greater market share taking place online. Global e-commerce sales are expected to rise to $2.4 trillion this year.

Morningstar Credit Ratings, a subsidiary of Morningstar, Inc., assessed the industrial sector in “an expansionary mode,” well-positioned, reporting, “Trends driving strong demand for warehouse space-primarily the growth of e-commerce and an expanding manufacturing sector-continue to drive low availability of space and encourage developers to build more.“

Their Chartbook report suggested with strong demand and low vacancies, industrial REITs in the first quarter easily increased rental rates. And while primary threats to these positive trends are a drop off in manufacturing activity (if escalating tariffs led to an outright trade war), or deceleration in e-commerce trends (very unlikely), the silver lining is: during the downside of previous cycles, the industrial sector “can turn off the new supply spigot relatively quickly, allowing supply and demand to more rapidly return to equilibrium.”

In a REIT.com article, Charles Keenan explains, “there is no doubt that one of the trends that has had the biggest impact on the real estate industry over the past decade has been the growth in e-commerce. While the rise in online shopping has clearly posed challenges for many retail real estate owners and tenants, it has been an absolute boon for other sectors-including industrial REITs.“

Monmouth Real Estate: An Overview

Monmouth Real Estate (MNR) is just a few years older than FedEx (NYSE:FDX) (Monmouth is in its 49th year as a public REIT), and the Industrial-sector REIT has also enjoyed a long-standing real estate relationship with the global shipping giant.

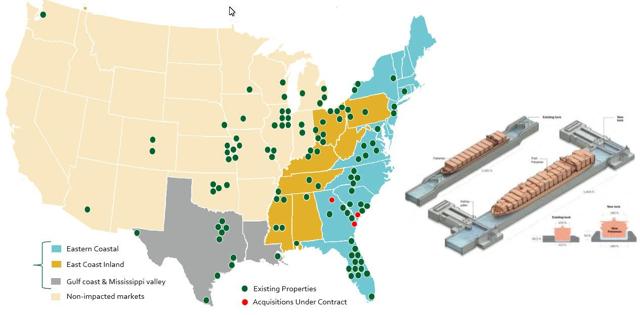

Monmouth operates a property portfolio that consists of 109 industrial properties, representing approximately 20.5 million square feet. The geographically diversified portfolio is from coast to coast across 30 states.

The portfolio is highly concentrated with FedEx; the remaining portfolio is balanced with high-quality tenants such as Siemens (OTCPK:SIEGY), Anheuser-Busch (NYSE:BUD), Caterpillar (NYSE:CAT), Coca-Cola (NYSE:KO), Kellogg (NYSE:K), Sherwin-Williams (NYSE:SHW), United Technologies (NYSE:UTX), Cracker Barrel (NASDAQ:CBRL), and others.

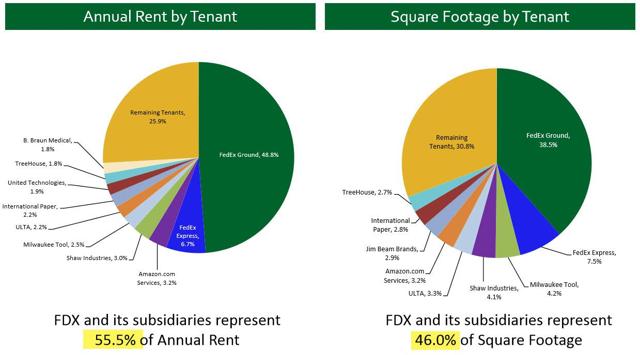

MNR began investing in properties leased to FedEx in 1992, and recent acquisitions include six properties consisting of an additional 1.8 million square feet leased to FedEx. Fourteen total expansion projects were recently completed, increasing the rent and lease terms of these FedEx facilities. FDX and its subsidiaries represent 55.5% of annual rent and 46.0% based on square footage.

Monmouth leases from FedEx Ground, FedEx Express, and FedEx Supply Chain Services – all unique operating subsidiaries that enjoy the parent S&P rating of BBB. On the Q4-18 earnings call, FedEx’s EVP, Raj Subramaniam commented:

“The economic outlook remains very favorable. The U.S. industrial sector has shifted into higher gear and capital spending is expanding. Consumers are benefiting from a strong labor market and tax cuts are supporting incomes.

Overall sentiment remains near multi-year highs. Globally, the structured three-speed world is becoming visible again after a couple of years of synchronous global growth. While the U.S. accelerates, the Eurozone and Japan are slowing and the emerging world continues to post the fastest rates of growth.

On balance, we expect another year of strong global growth as economic momentum runs through a healthy pace. Sound fundamentals remain in place to underpin sustained growth in global manufacturing and business investment.”

As you can see below, MNR also has substantial exposure to the East Coast, and that’s another important characteristic since the company should benefit from the Panama Canal expansion that was completed in the first half of 2016.

Each of MNR’s FedEx locations has become a highly coveted foothold for large businesses. Major retailers are drawn to FedEx locations, so they can get their goods delivered to their customers as fast as possible.

MNR’s FedEx Ground locations have become the nucleus of today’s logistics clusters. The company has focused investments on assets that are mission-critical to its strong tenant base.

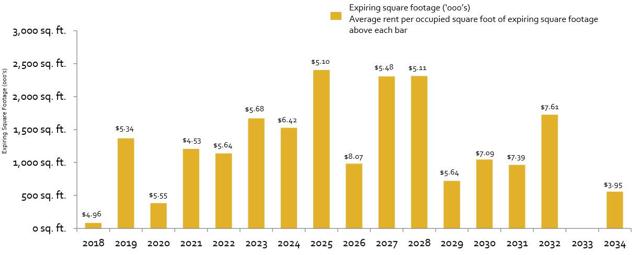

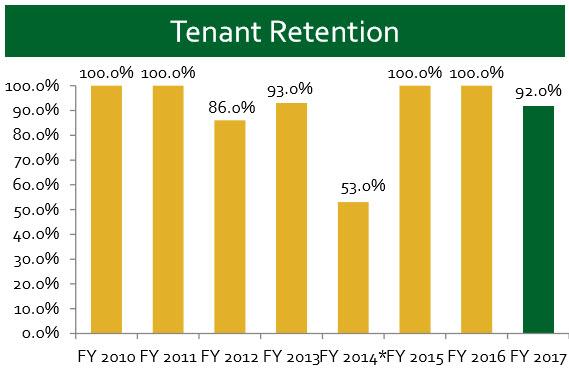

Note that the leases are well-balanced, so there is no fear of expirations that could impact MNR’s reliable rental income. Monmouth’s average lease maturity as of the latest quarter increased to 7.8 years and the average annual rent per square foot is $5.89.

During the latest quarter, Monmouth acquired two brand-new Class A built-to-suit facilities. These acquisitions contain a total of approximately 762,000 square feet and represent an aggregate cost of $64 million.

One of these acquisitions is leased to B. Braun Medical for 10 years and the other facility is leased to Amazon (NASDAQ:AMZN) for 11 years. From a run rate standpoint, Monmouth expects these two properties to generate a combined total annual rent of approximately $4.2 million, representing an initial unlevered return of 6.6%.

Monmouth financed both of these properties with two fixed-rate mortgages totaling $38.5 million with a weighted average interest rate of 4.2% and a weighted average debt maturity of 14.5 years. The B. Braun Medical facility located in Daytona Beach, Florida, near the tenant’s new manufacturing facility and is in close proximity to the Daytona Beach International Airport and Interstate 4.

The Amazon acquisition is located in Mobile, Alabama, and represents Monmouth’s second property leased to Amazon. The Port of Mobile has been experiencing substantial demand as a result of the recently completed Panama Canal expansion. With two interstate highway systems and five Class-1 railroads serving the port, this region is very well situated to benefit from meaningful long-term growth.

Thus far in fiscal 2018, Monmouth has acquired five buildings for a total purchase price of $174 million. Through the first three quarters, Monmouth has generated 9% growth in gross leasable area and a 15% increase over the prior-year period.

Additionally, during the quarter, Monmouth sold two properties totaling 156,000 square feet for net proceeds of approximately $11.6 million, resulting in a net realized gain of $2.1 million.

The Balance Sheet

Monmouth’s acquisition pipeline contains 1.1 million square feet, representing $221.4 million, comprised of four acquisitions scheduled to close over the next several quarters.

To take advantage of today’s attractive interest rate environment, Monmouth has already locked in very favorable financing for all four acquisitions. The combined financing terms for these four acquisitions consists of $142.1 million in proceeds, representing 64% of total cost, with the weighted average interest rate of 4.1%.

Each of the four financings are 15-year, self-amortizing loans and these acquisitions will result in a weighted average loans return on equity of approximately 13%.

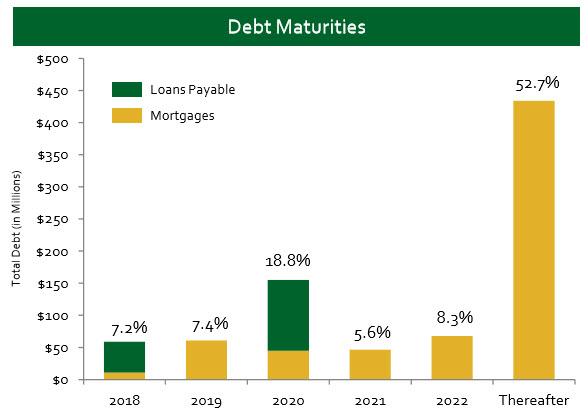

Thus far during fiscal 2018, Monmouth has fully repaid four mortgage loans, totaling approximately $8.6 million with fixed interest rates ranging from 5.2% to 6.8% associated with these properties. These newly unencumbered properties generate over $2.6 million in net operating income annually.

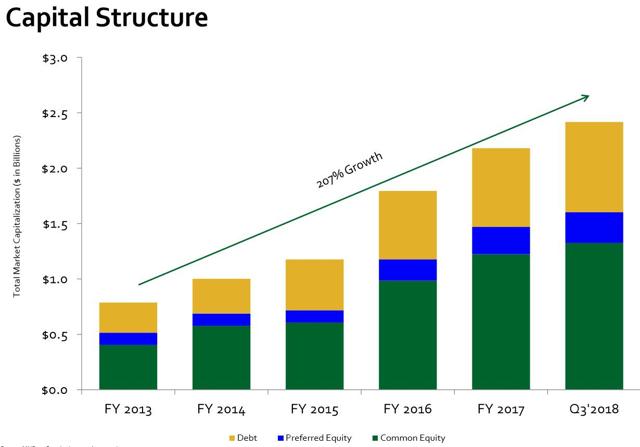

As of the end of the quarter, Monmouth’s capital structure consisted of approximately $815 million in debt of which $657 million was property level fixed-rate mortgage debt and $158 million were loans payable.

Around 81% of total debt is fixed rate, with the weighted average interest rate of 4.1% as compared to 4.2% in the prior-year period. Monmouth also had a total of $277 million in perpetual preferred equity at quarter-end. Combined with an equity market capitalization of $1.3 billion, the company’s total market capitalization was approximately $2.4 billion at quarter-end.

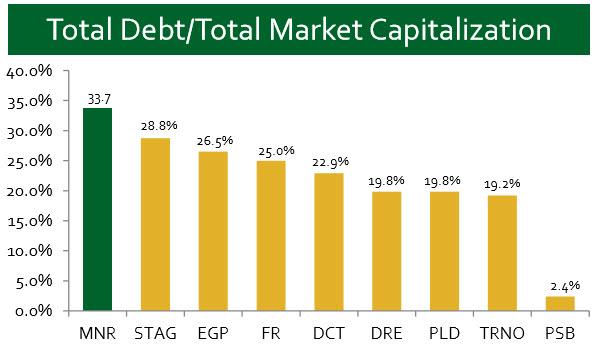

From a credit standpoint, Monmouth continues to be conservatively capitalized, with net debt to total market capitalization at 33%, and net debt plus preferred equity to total market capitalization at 45% at quarter-end.

In addition, Monmouth’s net debt less securities to total market capitalization was 26% and net debt less securities plus preferred equity to total market capitalization was 38% at quarter-end.

For the three months ended June 30, 2018, Monmouth’s fixed charge coverage was 2.4x, and net debt to EBITDA was 6.6x. The ratio of net debt less the REIT securities portfolio to EBITDA was 5.2x.

From a liquidity standpoint, Monmouth ended the quarter with $6.9 million in cash and cash equivalents and held $167.6 million in marketable REIT securities with $8.4 million in unrealized losses.

At quarter-end, Monmouth’s $167.6 million REIT securities portfolio represented 9.2% of undepreciated assets. Additionally, the company had $90 million available from the credit facility as of the quarter-end, as well as an additional $100 million potentially available from the accordion feature.

The Latest Earnings Results

Monmouth’s core funds from operations for Q3-18 were $18 million, or $0.23 per diluted share. This compares the core FFO for the same period one-year ago of $15.4 million or $0.21 per diluted share, representing an increase of 10%.

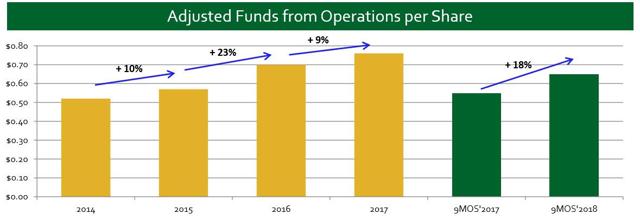

Adjusted funds from operations (or AFFO, which excludes security gains or losses) was $0.22 per diluted share for the recent quarter, representing an increase of 16% over the prior-year period.

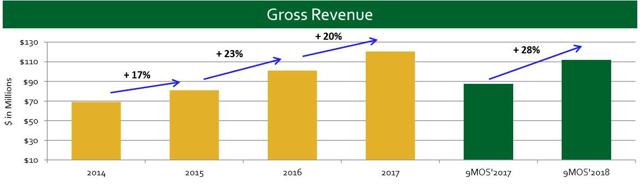

Rental and reimbursement revenues for the quarter were $36.2 million, compared to $28.6 million, or an increase of 27% from the prior year. Net operating income increased $4.8 million to $28.8 million for the quarter, reflecting a 20% increase from the comparable period a year ago.

This increase was due to the additional income related to the 10 properties purchased during fiscal 2017, and the 5 properties purchased during the first three quarters of fiscal 2018.

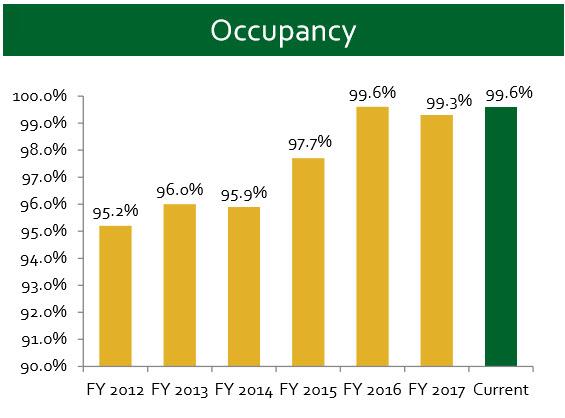

Monmouth’s end of period occupancy decreased 20 basis points from 99.8% in the prior-year period to 99.6% at quarter-end, and was up 40 basis points sequentially. As referenced above, the weighted average lease maturity as of the quarter-end was 7.8 years, which remained unchanged from the prior-year period.

With regards to Monmouth’s same property metrics for the current nine-month period, the same property occupancy decreased 30 basis points from 99.8% to 99.5%, while same property NOI remained relatively unchanged.

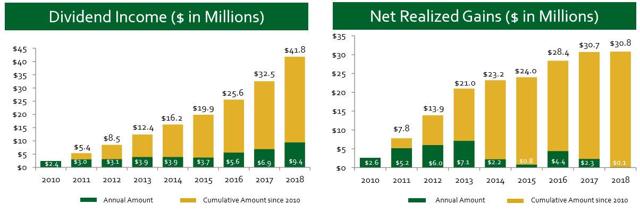

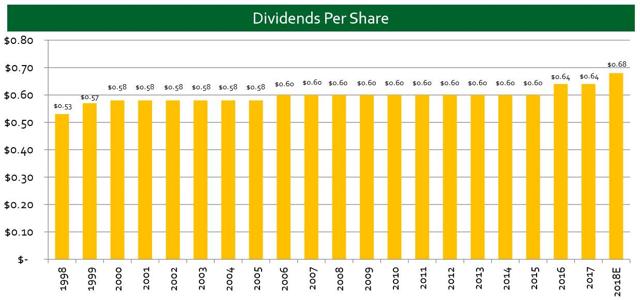

Monmouth has maintained or increased its common stock dividend for 26 consecutive years, and also increased AFFO per share by 16% over the prior-year quarter and by 18% year over year for the nine-month period.

As Monmouth’s CEO, Mike Landy points out:

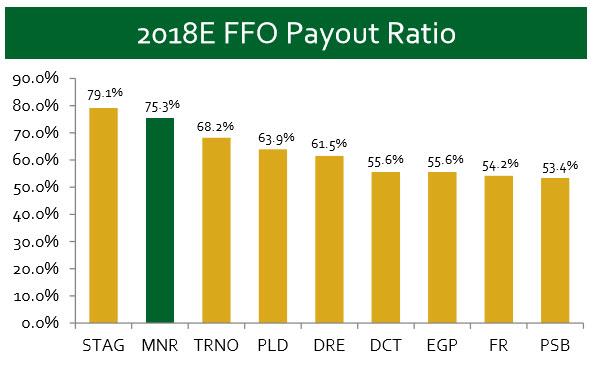

“With a very conservative 77% AFFO dividend payout ratio this quarter, we remain confident about continuing to provide our shareholders with the high-quality, reliable income streams we have delivered for over a quarter century. This quarter represented our 10th consecutive quarter with an occupancy rate above 99%.”

The Key Differentiator

It’s important to understand that while Monmouth is considered an Industrial REIT, the company has longer lease terms than many of the peers. Most industrial leases are 5 years (with options to extend), but Monmouth invests in newer buildings that were build-to-suit for companies like Amazon and FedEx.

These newer buildings make Monmouth more like a Net Lease REIT than an Industrial REIT, and this means there is less cap-ex and releasing costs (compared to the industrial REIT peers).

So there is value in Monmouth’s highly predictable cash flows that are less influenced by tenant rollover and retention risk. Now consider Monmouth’s attractive dividend history:

As you will see, Monmouth has not excelled at dividend growth, up until recently. However, it’s important to note that the company has never cut its dividend.

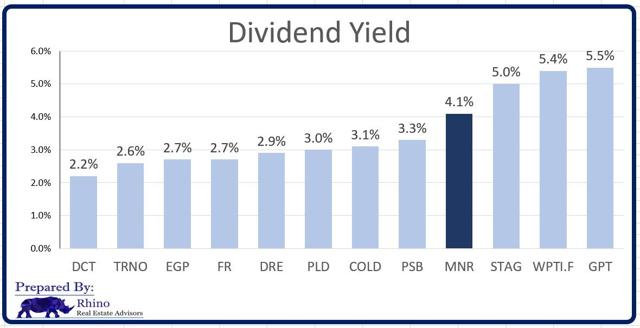

Now let’s compare Monmouth’s dividend yield with the peer group:

Considering Monmouth’s growing portfolio of high-quality properties, I consider the dividend yield attractive. Remember that the payout ratio is now 77% (based on AFFO) that provides a nice cushion and attractive margin of safety supporting continued acceleration of dividend growth. Now consider the P/FFO multiple:

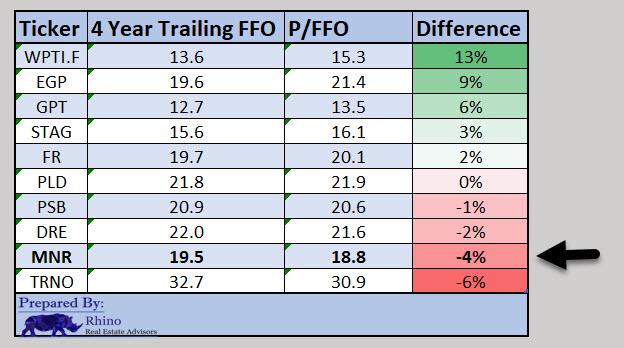

As you can see, many of the Industrial REITs have benefitted from the boom, but Monmouth continues to trail the 4-year P/FFO average. Currently, Monmouth trades at 18.8x, around 4% below the 4-year average.

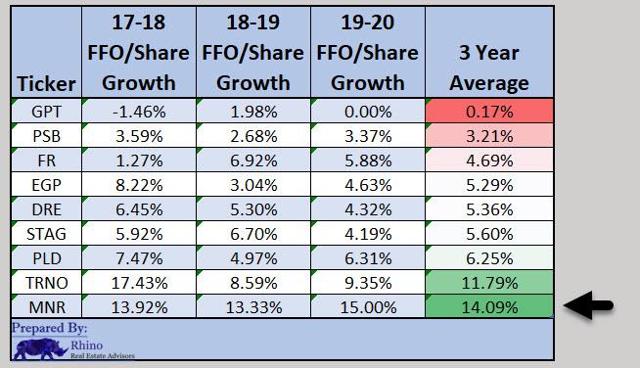

What about growth?

As you see, Monmouth is forecasted to grow FFO/share by double digits in 2018-2020. There aren’t many REITs that can move the needle by double digits unless you are in the cell tower or data center sector.

Wait… Monmouth is in the e-commerce sector and that’s precisely what is fueling the strong performance.

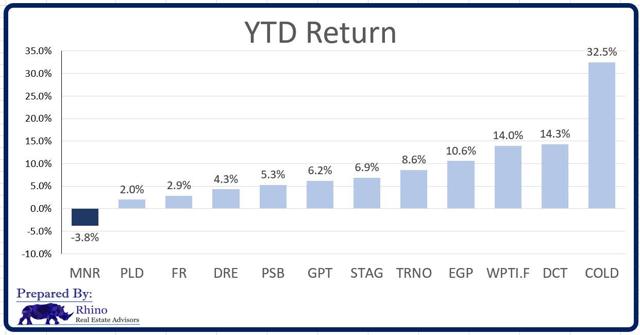

So why has Mr. Market ignored the catalyst?

I can’t speak for Mr. Market, but I can for myself…

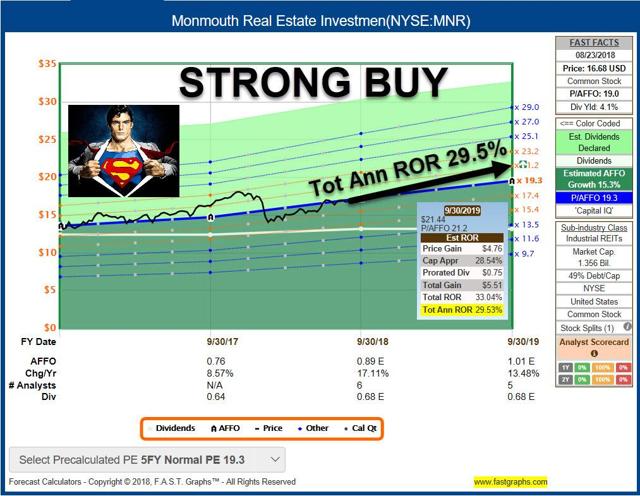

I am upgrading Monmouth from a BUY to a STRONG BUY and including this REIT in my “New Money Portfolio“. Essentially, this means that I believe Monmouth could generate total returns of around 25% per year during 2018 and 2019. For more information on the New Money portfolio, subscribe to The Intelligent REIT Investor or the Forbes Real Estate Investor newsletter.

Note: Brad Thomas is a Wall Street writer, and that means he is not always right with his predictions or recommendations. That also applies to his grammar. Please excuse any typos, and be assured that he will do his best to correct any errors, if they are overlooked.

Finally, this article is free, and the sole purpose for writing it is to assist with research, while also providing a forum for second-level thinking. If you have not followed him, please take five seconds and click his name above (top of the page).

Sources: F.A.S.T. Graphs and MNR Investor Presentation.

Each week, Brad provides Marketplace subscribers with actionable REIT news, including (1) Friday afternoon subscriber calls, (2) Weekender updates, (3) Google portfolios, (4) Real-time alerts, (5) Early AM REIT news, (6) chat rooms, (7) the monthly newsletter, and (8) earnings results in Google Sheets.

Marketplace subscribers have access to a wide range of services, including weekly property sector updates and weekly Buy/Sell picks. We provide most all research to marketplace subscribers, and we also provide a “weekender” report and a “motivational Monday” report. We stream relevant real-time REIT news so that you can stay informed.

All of our portfolios are updated daily, and subscribers have access to all of the tools via Google Sheets. REITs should be part of your daily diet, and we would like to help you construct an Intelligent REIT portfolio, utilizing our portfolio modeling strategies. Brad reminds all subscribers and prospective subscribers that “the safest dividend is the one that’s just been raised.”

Disclosure: I am/we are long ACC, AVB, BHR, BPY, BRX, BXMT, CCI, CHCT, CIO, CLDT, CONE, CORR, CTRE, CXP, CUBE, DEA, DLR, DOC, EPR, EQIX, ESS, EXR, FRT, GDS, GEO, GMRE, GPT, HASI, HT, HTA, INN, IRET, IRM, JCAP, KIM, KREF, KRG, LADR, LAND, LMRK, LTC, MNR, NNN, NXRT, O, OFC, OHI, OUT, PEB, PEI, PK, PSB, PTTTS, QTS, REG, RHP, ROIC, SBRA, SKT, SPG, SRC, STAG, STOR, TCO, TRTX, UBA, UMH, UNIT, VER, VICI, VNO, VNQ, VTR, WPC.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.