Gold weathered the Federal Reserve’s 7th rate hike of this cycle this week. Gold-futures speculators and to a lesser extent gold investors have long feared Fed rate hikes, selling ahead of them. Higher rates are viewed as the nemesis of zero-yielding gold. But contrary to this popular belief, past Fed rate hikes have proven very bullish for gold. This latest hike once again leaves gold set up for a major rally in coming months.

The Fed’s Federal Open Market Committee meets 8 times per year to make monetary-policy decisions. These can really impact the financial markets, and thus are closely watched by gold-futures speculators. These elite traders wield wildly-outsized influence on short-term gold price action due to the truly extreme leverage inherent in gold-futures trading. What they do before and after FOMC decisions really impacts gold.

This week’s latest Fed rate hike was universally expected. Trading in the federal-funds-futures market effectively implies rate-hike odds. Way back in mid-April they shot up to 100% for this week’s meeting, then stayed there for 5 weeks. In the last several weeks they averaged 91%. So everyone knew another Fed rate hike was coming. That’s typical, as the FOMC doesn’t want to surprise the markets and ignite selloffs.

The big unknown going into the every-other FOMC meetings followed by press conferences from the Fed chairman is the future rate-hike outlooks. Top FOMC officials’ individual federal-funds-rate outlooks are summarized in a chart traders call the “dot plot”. That was hawkish this week, with 2018’s total expected rate hikes climbing from 3 to 4. More near-term rate hikes projected have really hammered gold in the past.

But on this week’s Fed Day gold didn’t plunge despite these hawkish dots and 7th rate hike of this cycle. Gold was around $1297 as the FOMC statement and dot plot were released that afternoon, and only fell modestly to $1293 after that. Then it started rallying back a half-hour later during Jerome Powell’s post-decision press conference. Gold closed that day at $1299, actually rallying 0.3% through a hawkish FOMC.

Gold-futures speculators usually sell leading into the every-other “live” FOMC meetings with dot plots and press conferences. Incidentally the first thing the new chairman Powell discussed this week is he is going to begin holding press conferences after all 8 FOMC meetings each year starting in January! So the gold-futures-driven gold volatility surrounding the Fed could very well become more frequent in 2019 and beyond.

All that gold-futures selling before FOMC meetings leaves speculators’ positions too bearish. And the Fed tries hard to never majorly surprise on the hawkish side anyway. So after FOMC decisions the very gold-futures speculators who sold aggressively leading into them often start buying back in. This trading dynamic forces gold lower leading into Fed Days, and then drives big rebound rallies coming out of them.

This week a single gold-futures contract controlling 100 troy ounces of gold worth about $130,000 had a maintenance-margin requirement of just $3100! So futures traders can run up to 41.9x leverage to gold, which is mind-boggling. The legal limit in the stock markets has been 2x for decades. At 40x each dollar deployed in gold futures has 40x the impact on the gold price as another dollar invested in gold outright.

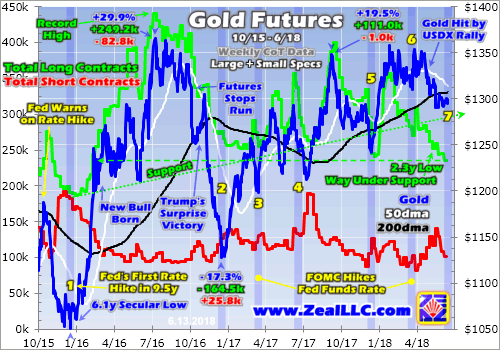

So even if you don’t trade gold futures like the vast majority of gold investors, they are important to watch since they dominate short-term gold action. This first chart looks at gold and speculators’ total long and short positions in gold futures over this Fed-rate-hike cycle. Each of these 7 rate hikes is highlighted, showing how gold sells off into them before rallying out of them mostly driven by speculators’ gold-futures trading.

Back in late 2015, the FOMC hadn’t hiked its FFR for nearly a decade. At its late-October 2015 meeting, the FOMC statement warned the Fed was “determining whether it will be appropriate to raise the target range at its next meeting”. That hawkish signal shocked gold-futures traders and they started dumping long contracts while rapidly ramping short sales. Gold was crushed on that, falling 9.1% over the next 7 weeks.

On the eve of that fateful mid-December FOMC decision to start hiking rates again for the first time in 9.5 years, everyone was convinced that was bad news for gold. Gold yields nothing, so surely higher bond yields would divert investment away from gold. It sounds logical, but history has proven the opposite. So just days before that initial Fed rate hike, I wrote a bullish essay showing how gold thrived in past rate-hike cycles.

Gold surged 1.1% the day of that first hike, but plunged 2.1% to a 6.1-year secular low of $1051 the very next day. Foreign traders had fled overnight following that rate hike. But gold started powering higher right after that. By mid-February 2016 gold had roared back up 18.5% on all that post-FOMC-rebound spec long buying and short covering! Gold formally entered a new bull market at +20% a few weeks later.

The Fed’s second rate hike of this cycle came exactly a year after the first in mid-December 2016. Again the Fed telegraphed another hike, so again gold-futures speculators fled longs and ramped shorts. In the 5 weeks leading into that FOMC meeting, gold plunged 11.2%. That was really exacerbated by the extreme Trumphoria stock-market rally in the wake of Trump’s surprise election victory early in that same span.

While everyone saw that Fed hike coming, the dot-plot rate-hike outlook of top FOMC officials climbed from 2 additional rate hikes in 2017 to 3. So spec gold-futures selling exploded, battering gold 1.4% lower that day and another 1.2% to $1128 the next. That hawkish FOMC surprise of more rate hikes faster was the worst-case Fed-decision scenario for gold. The general gold bearishness was epically high.

But gold didn’t plunge from there like everyone expected. Instead it rebounded dramatically higher with an 11.4% rally over the next 10 weeks or so! When speculators’ gold-futures longs get too low and/or their shorts get too high heading into any FOMC decision, these excessive trades have to be reversed in its wake. Any pre-FOMC gold-futures selling directly translates into symmetrical post-FOMC buying.

Since the FOMC spaced out its initial couple hikes of this cycle by an entire year, there was rightfully a lot of skepticism about when the third would come. So up until just a couple weeks out from the mid-March-2017 FOMC meeting, the FF-futures-implied rate-hike odds were just 22%. But Fed officials jawboned them up to 95% by a couple days before that meeting. Gold was again hit on Fed-rate-hike fears, falling 4.7%.

But right after that third rate hike of this cycle, gold immediately caught a bid and surged 7.6% higher over the next 5 weeks or so. That dot plot kept the 2017 rate-hike outlook at 3 total, not upping it to 4 as the gold-futures speculators expected. So again they were forced to admit their pre-FOMC bearishness was way overdone and buy back in. Fed rate hikes aren’t bearish for gold despite traders’ irrational expectations.

After being wildly wrong for three Fed rate hikes in a row, some of the gold-futures speculators started to pay attention heading into this cycle’s 4th hike in mid-June 2017. But gold still fell 2.1% over several trading days leading into it. That hike too was universally expected like nearly all of them, and the dot plot was neutral staying at 3 total hikes in 2017. But the gold-futures selling broke precedent to continue that time.

In the first week or so after that 4th hike last summer, gold fell 1.9%. Those post-hike losses extended to 4.2% total by early July. That particular rate hike was unique to that point in that it came to pass early in gold’s summer doldrums. In June and early July, gold investment demand wanes so it usually just drifts sideways to lower. Thus this decades-old seasonal lull effectively delayed that post-FOMC gold reaction rally.

Once last year’s summer-doldrums low passed, gold again took off like a rocket as specs scrambled to normalize their excessively-bearish gold-futures bets. So gold surged 11.2% higher between early July and early September on heavy gold-futures buying. This gold reaction to last June’s 4th Fed rate hike may be the best template of what to expect after this June’s 7th one. Summer may again delay gold’s rebound.

But whether gold’s usual post-FOMC rally starts now or a few weeks from now is ultimately irrelevant in the grand scheme. The seasonally-weak summer doldrums don’t change the fact that speculators’ gold-futures bets get too extreme heading into telegraphed Fed rate hikes, so they have to be normalized in the FOMC’s wake. This gold-bullish pattern has held true to varying degrees after all 6 previous hikes of this cycle.

The Fed took a break from hiking in September 2017 to announce its wildly-unprecedented quantitative-tightening campaign to start to unwind long years and trillions of dollars of QE money printing. So the rate hikes resumed at that every-other-FOMC-meeting tempo in mid-December 2017. Again the goofy gold-futures traders started fearing another hawkish dot plot, so gold fell 4.0% in several weeks leading in to it.

But that 5th rate hike of this cycle was accompanied by a neutral dot plot forecasting 3 more rate hikes in 2018 instead of the 4 gold-futures traders expected. So again they had to admit their bearishness was way overdone and buy back in aggressively. So over the next 6 weeks after that FOMC meeting, gold shot 9.2% higher to $1358 nearing a major breakout! How can anyone believe rate hikes are bearish for gold?

The 6th hike of this cycle came right on schedule in late March this year, accompanied by a neutral dot plot still forecasting 3 total rate hikes in 2018. But again the gold-futures traders worried leading into that FOMC decision, pushing gold 3.2% lower over the prior month or so. They started buying back in that very Fed Day, so gold sharply rebounded 3.3% higher to $1353 within 4 trading days of that Fed rate hike.

This gold-futures-driven gold price action surrounding Fed rate hikes is crystal-clear. Gold falls leading into FOMC meetings with expected hikes on fears of hawkish rate-hike forecasts in the dot plots. All that pre-FOMC selling leaves speculators’ collective gold-futures bets way too bearish, with longs too low and/or shorts too high. Then once the Fed acts and specs realize gold isn’t collapsing, they quickly buy back in.

The Fed’s again-universally-expected 7th rate hike of this cycle came this Wednesday. And despite the gold-bullish examples of all the prior 6 hikes, gold-futures traders again sold leading into it. Starting back in mid-April, they embarked on a major long liquidation that pushed gold 4.0% lower by this week’s FOMC eve. In their defense that was mostly in response to a US dollar short squeeze, so maybe they are learning.

Gold-futures data is released weekly in the CFTC’s famous Commitments of Traders reports. These are published late Friday afternoons current to preceding Tuesday closes. So the latest data available when this essay was published is from the CoT week ending June 5th. Even then a week before this 7th Fed rate hike, total spec longs at 235.9k contracts were way down at a 2.3-year low! Speculators were all out.

The Fed indeed hiked as expected, and specs’ hawkish forecast seemed to be confirmed by this newest dot plot. Finally at this week’s FOMC meeting the collective rate-hike outlook rose from 3 total hikes in 2018 to 4. That was the perfect excuse for gold-futures traders irrationally terrified of higher rates to sell gold hard! Yet they couldn’t, with their longs among the lowest levels of this bull the selling was already exhausted.

So gold is once again set up with a very-bullish June-rate-hike scenario like last summer. Once again specs need to normalize their collective gold-futures bets after waxing too bearish leading into another Fed rate hike. That big gold-futures buying is inevitably coming, although it may once again be delayed for a few weeks by the summer doldrums. That would simply add to gold’s powerful seasonal autumn rally.

Gold’s resilience this week in the face of that hawkish dot plot was very impressive. Remember the last time the near-term FFR forecast added another hike in mid-December 2016, gold plunged 2.6% in only 2 trading days. The fact gold didn’t suffer another kneejerk plunge this week on adding another hike this year shows considerable strength! Speculators could’ve aggressively short sold gold futures, but refrained.

Thus gold’s post-rate-hike reaction after this 7th one is likely to mirror the strong rallies after the prior 6. They ranged from 3.3% to 18.5% in the weeks and months after hikes, averaging 10.2%. Given we’re in the heart of the summer doldrums, gold’s post-FOMC rally this summer could mirror last summer’s. It didn’t start until early July, but from there gold blasted 11.2% higher into early September. That’s a big deal.

Gold was trading at $1295 this Tuesday before this week’s FOMC decision. That’s a high base relative to gold’s bull-to-date peak of $1365 from early July 2016. A decisive 1% breakout above that happens at $1379. That would change everything for gold psychology, unleashing a major new wave of global gold investment demand. That critical breakout level for sentiment is only 6.4% above this week’s FOMC-eve close!

So there’s a good chance this coming 7th post-rate-hike rally of this gold bull will push gold’s price into major-breakout territory! As long as gold doesn’t slump too deep in the remaining summer doldrums of the next few weeks, that targets a potential breakout span in this year’s autumn rally. Those tend to peak by late September. With gold relatively high and spec gold-futures longs super-low, gold’s setup is very bullish.

For 7 Fed rate hikes in a row now, most traders have believed and argued that higher rates are bearish for gold. This rate-hike cycle is now 2.5 years old, plenty of time for that popular thesis to play out. Yet between the day before that first hike in mid-December 2015 and this week’s 7th hike, gold still rallied 22.4% higher! The US Dollar Index, which was supposed to soar on rate hikes, slipped 4.7% lower in that span.

Conventional wisdom on Fed rate hikes is obviously very wrong. That’s nothing new, as my extensive research has documented. Throughout all of modern history, gold has thrived during Fed-rate-hike cycles. Today’s cycle is the 12th since 1971. During the exact spans of all previous 11, gold averaged a solid 26.9% gain. During the 6 of these where gold rallied, its average rate-hike-cycle gain was a huge 61.0%!

The Fed’s last rate-hike cycle ran from June 2004 to June 2006, dwarfing today’s. The FOMC hiked in 17 consecutive meetings, totaling 425 basis points which more than quintupled the FFR to 5.25%. If rate hikes and higher rates are bad for gold, it should’ve plummeted at 5%+. But instead gold surged 49.6% higher over that exact span! Fed-rate-hike cycles are bullish for gold, regardless of what futures guys think.

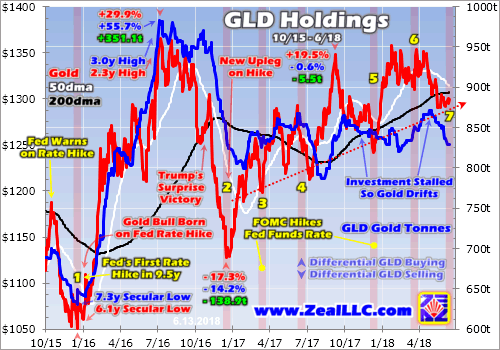

Sadly their irrational and totally-wrong bearish psychology even infects gold investors. This next chart looks at gold and the physical gold bullion held in trust for GLD shareholders. That is the world’s largest and dominant gold ETF (GLD). Its holdings reflect gold investment trends, rising when capital is flowing into gold and falling when investors are leaving. That futures-driven gold action around rate hikes is affecting investment!

Unfortunately this essay would get far too long if I dive deeply into this chart. But I couldn’t exclude it from this discussion either. Because of that goofy gold-futures trading action surrounding Fed rate hikes in this cycle, investors have followed suit to varying degrees. They tend to sell gold leading into Fed rate hikes, and that downside momentum often continues in the weeks after hikes. That really weighs on gold.

But after a couple weeks of strong post-FOMC rallying driven by that gold-futures rebound buying, investors once again start warming to gold. They resume buying GLD shares faster than gold itself is being bought, and start amplifying gold’s post-rate-hike rallies after retarding them initially. It is disappointing that investors too are drinking the psychological tainted Kool-Aid poured by gold-futures speculators.

As a battle-hardened speculator myself and lifelong student of the markets, I don’t care which way they are going. We can trade them up or down and make money. But it’s very frustrating when the traders who dominate gold’s short-term price action continue to cling to a myth, distorting signals and misleading everyone else. History has proven over and over again that Fed-rate-hike cycles are very bullish for gold.

Gold has rallied strongly on average after 6 of the past 6 Fed rate hikes of this cycle! Last summer was the only quasi-exception, when gold’s weak seasonals delayed its post-hike rally for a few weeks. There is literally no reason not to expect gold to power higher again after this week’s 7th hike. And with gold at these levels, that next post-FOMC rally should see a major bull-market breakout that will bring investors back.

The last time investors flooded into gold in early 2016 after that initial December rate hike, gold powered 29.9% higher in 6.7 months. The beaten-down gold miners’ stocks greatly amplified those gains, with the leading HUI gold-stock index soaring 182.2% higher over roughly that same span! Gold stocks are again deeply undervalued relative to gold, a coiled spring ready to explode higher in this gold bull’s next major upleg.

The bottom line is Fed rate hikes are bullish for gold, and this week’s is no exception. Gold has not only powered higher on average in past Fed-rate-hike cycles, but has rallied nicely in this current one. Gold enjoyed big rebound surges after all 6 previous Fed rate hikes of this cycle. Gold-futures speculators who sold too aggressively leading into FOMC meetings had to buy back after to normalize their bearish positions.

And gold looks super-bullish in the coming months after this week’s 7th Fed rate hike of this cycle. Those gold-dominating futures traders sold their longs down to levels not seen since the initial months of this gold bull! So they’re going to have to do huge buying to reestablish normal positioning. While gold’s summer doldrums may delay that a few weeks, the coming gold-futures buying could drive a major upside breakout.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I own extensive long positions in gold stocks and silver stocks which have been recommended to our newsletter subscribers.