In part 2 of our “Congratulations, Your Income Is Too High” series, we continue our examination of non-deductible IRA contributions. In the first part of the series, we analyzed the merits of making after-tax contributions into a Traditional IRA. The benefits of trading annual taxes on investment income for deferred taxes with a built-in future income tax liability is highly dependent upon an individual’s circumstances and portfolio allocation.

In this article, we will dive deeper into the benefits of converting Traditional IRAs that contain after-tax money to a Roth IRA. We will also explore methods to minimize the tax impact of the Roth conversion process when pre- and post-tax monies are commingled in a Traditional IRA. The overall theme of part 1 and part 2 is to minimize the drag of taxes to maximize portfolio values. Investors are only allowed to keep what the government leaves behind and intelligent tax management can improve returns.

We will continue to follow Mr. Legume, who in no way, shape or form is similar to Mr. Peanut, as he journeys from his 40s to his 70s. Mr. Legume is single, 40 years of age, has a MAGI of $125,000, and is in the 24% tax bracket now and in retirement. Mr. Legume earns too much to contribute to a Roth IRA, and his income is too high to deduct contributions into his Traditional IRA account. He will make after-tax contributions of $5,500 ($6,500 after 50 years of age) until he reaches the age of 65. A total of $159,000 in after-tax money will be contributed over this 25-year period.

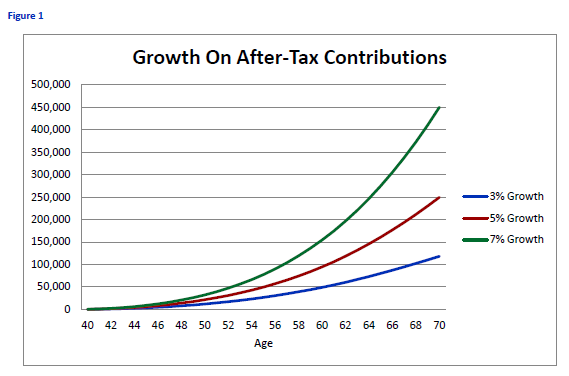

Although Mr. Legume will not have to pay tax again on the $159,000 in after-tax contributions into the Traditional IRA, he will have to pay income tax on its growth. Figure 1 below outlines the growth on these after-tax contributions in 3%, 5%, and 7% return scenarios. The growth on the annual after-tax contributions is ~$118,000, ~$249,000, and ~$450,000 under the 3%, 5%, and 7% return scenarios, respectively. This growth is subject to income taxes when it is withdrawn in retirement.

The chart illustrates the unremarkable fact that higher rates of return lead to more growth. However, hidden within the chart is a built-in tax liability of income tax on this growth. The after-tax value of a Traditional IRA is equal to:

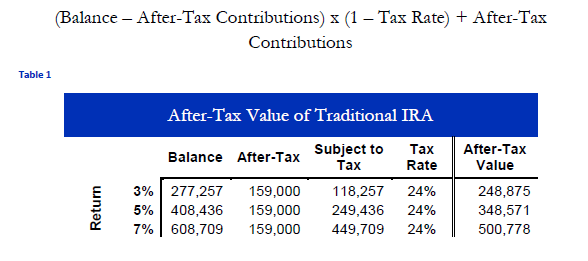

Table 1 above outlines the after-tax value of Mr. Legume’s Traditional IRA when he reaches 70 years of age. Even in the low return environment, Mr. Legume’s account will have a built-in tax liability of ~$28,000. In the 7% return scenario, Mr. Legume’s tax liability is ~$108,000. The built-in tax liability of Traditional IRAs is significant, especially considering that after-tax monies were utilized. Converting these after-tax Traditional IRA contributions to a Roth IRA provides a tremendous amount of future tax savings.

Prior to 2010, there were income restrictions in place that prevented high earners from converting Traditional IRAs to Roth IRAs. Fortunately, Congress in 2010 passed legislation that removed income restrictions that prevented Roth conversions for those making too much money. This opened a “back-door” for Roth contributions: make a non-deductible Traditional IRA contribution and immediately convert to a Roth IRA. After-tax contributions are not taxed when converted to a Roth and the immediate conversion avoids income taxes on the growth.

However, the IRS does not serve free lunch. The IRS requires that a proportionate amount of pre- and post-tax money be converted. An investor cannot just choose to convert the post-tax monies. For detailed information on the Backdoor Roth conversion process please read my article Keep The Backdoor Roth IRA Open. Effectively, pre-tax money inside of an IRA (Traditional, SEP, or SIMPLE) makes the conversion process less efficient as it creates a tax drag.

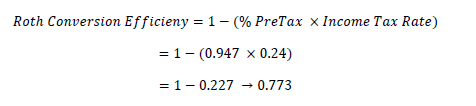

According to Fidelity’s Retirement Analysis[i] the average balance in IRA and 401(k) accounts at the end of the third quarter of 2017 was $103,500 and $99,900, respectively. Assuming Mr. Legume has the average IRA account balance, we will explore that tax drag on converting to a Roth IRA.

Mr. Legume would pay income tax on ~95? of every dollar converted. Effectively, 77? of every dollar would get converted into the Roth IRA.

If Mr. Legume converted $10,000 to a Roth IRA, he would owe ~$2,272 in taxes. If Mr. Legume followed the typical financial advice of rolling his old 401(k) or 403(b) plan into his IRA, his Roth conversion efficiency would decline.

In this case, a $10,000 conversion would result in ~$2,332 in taxes.

Ideally, the tax would be paid with money outside of the IRA account to maximize the amount going into the Roth IRA account. However, this tax drag can be reduced by keeping money inside of old 401(k)plans. In an ideal situation, Mr. Legume would have no pre-tax money inside of an IRA account and the conversion efficiency would be dollar for dollar.

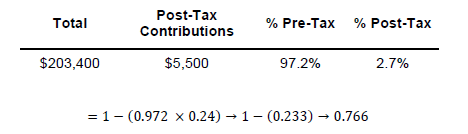

Moving forward, we will assume Mr. Legume rolled previous 401(k) plan assets into his IRA. The account is currently 97% pre-tax money and 3% after-tax contribution. There are a couple of additional methods for offsetting the tax drag on his contributions: salary deferral into the 401(k) and funding an HSA account.

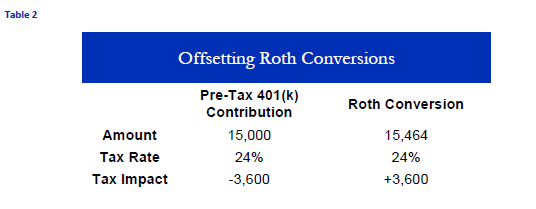

The first one would be to utilize pre-tax contributions into a 401(k) or 403(b) plan to offset the Roth conversion amount. For example, Mr. Legume could defer $15,000 of his salary into his company’s 401(k) plan. This would reduce his taxes by $3,600. In the same year, he could convert $15,464 (15,000 / 97%) of his Traditional IRA to a Roth. This would increase his taxes by $3,600. This offers no current tax benefit, but reduces the future tax liability on the after-tax Traditional IRA contributions.

It is important to note that while salary deferral into SIMPLE IRAs lowers taxes, these deferrals also increase the amount of pre-tax money in IRA accounts, thus increasing the amount subject to income tax on conversion. Balances in Traditional, Rollover, SEP and SIMPLE IRAs count in the pro-rata calculation. In addition, it is the balance in these accounts as of December 31st that is used. So if an investor did a Roth conversion in February and then rolled a 401(k) plan into an IRA in September, this would increase the amount of money subject to taxation on the conversion. The IRS charges for lunch – it is not free.

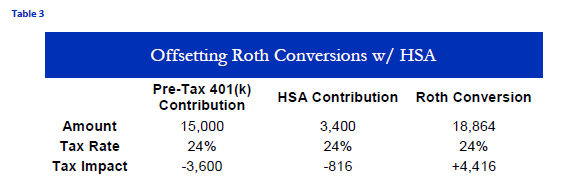

Health Savings Accounts (HSAs) provide another tool to reduce the tax drag on Roth conversions. Contributions into HSA accounts are tax deductible. For 2017, an individual can contribute up to $3,400 and a family can put in up to $6,750. There is a catch-up contribution of $1,000 for those 55 years of age or older. Table 3 below expands upon the offsetting Roth conversions from just utilizing 401(k) contributions.

As illustrated in Tables 2 and 3, utilizing tax-deductible contributions into 401(k) plans and HSA accounts can offset the tax drag caused by Roth conversions when there are pre-tax monies in IRA accounts. This in turn reduces the future tax liability of Traditional IRA accounts. As we have seen in Figure 1, this growth on after-tax money is significant over time.

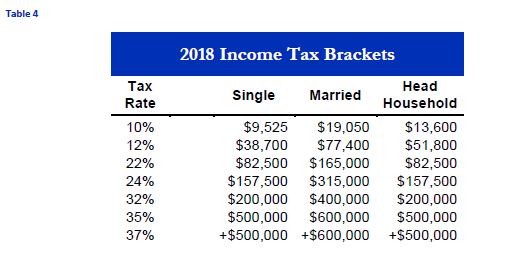

Another point of consideration to decrease the amount of time post-tax money spends in the Traditional IRA account is to convert an additional sum of money up to the next highest tax bracket. In the case of Mr. Legume, he would have an additional $32,500 that could be converted and still remain in the 24% tax bracket. However, this would increase taxes by $7,800. This trade-off is not likely worth the expense especially if the money is instead invested in a tax efficient manner. Table 4 below outlines the income tax brackets for 2018:

The goal of converting after-tax money to a Roth is to reduce the future tax liability on these taxed contributions. The IRS only allows one to defer taxes for so long prior to demanding their share. In the year a person turns 70.5 years of age, the IRS requires distributions from Traditional IRA accounts. These forced withdrawals from Traditional IRA accounts count as income. Depending upon the size of the retirement accounts, these can be sizeable distributions. Roth conversions reduce the balance of IRA accounts, which in turn reduces the required distribution amount. Distributions from Roth IRAs are not subject to tax and do not count as income.

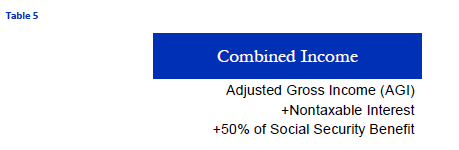

This lengthy explanation leads to taxability of Social Security. By the time the IRS demands a piece of Traditional IRAs, investors will be drawing Social Security. If a person’s “combined income” is above a certain threshold, a portion of Social Security is subject to tax.[ii] Table 5 below is the calculation for “combined income”. Distributions from Traditional IRAs are accounted for in the AGI.

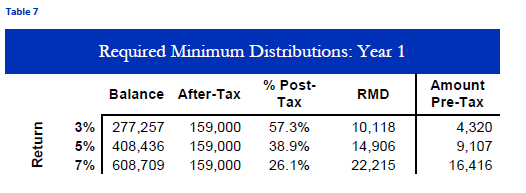

Returning to the data from Table 1, the table below outlines the required minimum distribution (RMD) that Mr. Legume would have to take in his first year. In the year an investor turns 70.5 years of age, the IRS requires a distribution from the IRA account. In year 1, the account value is divided by 27.4 to arrive at the RMD. The last column on the table is the amount of pre-tax money that is subject to income tax and thus is added to adjusted gross income (AGI).

If we assume Mr. Legume receives $2,000 per month in Social Security, this only leaves $13,000 of AGI or non-taxable interest before 50% of his Social Security is subject to income tax. If he was able to average a return of 7%, 50% of his Social Security would already be subject to taxation. This reduces his Social Security benefit to $1,760 after tax (50% X $2,000 X 24%).

Making after-tax conversions, even with pre-tax money in the account, reduces future adjusted gross income. The decision to make a non-deductible contribution or to invest in a taxable account is highly dependent upon an individual’s circumstances, current and future. In part 1, we evaluated in isolation the trade-off between deferred income tax and annual investment taxes. We conclude in this situation that after-tax contributions should be made if the monies are going to be generally invested in a tax-inefficient manner. Otherwise the higher income tax more than offsets the benefits of tax deferral on tax efficient investments.

Advancing one more step, if an investor has a 401(k) or 403(b) plan, this improves the efficiency of converting after-tax contributions to a Roth as the income reduction from deferral can offset the income increase from conversion. This in turn can reduce adjusted gross income in retirement by reducing required distributions amounts and possibly the amount of Social Security subject to tax.

As with any general investment advice, the above is too generic to be correct on an individual level. We urge you to take this framework and modify it to maximize your individual situation. The important take is to consider current and future tax implications to maximize portfolio values as the 636 elected officials will only allow you to keep what they do not take.

We hope our this article is helpful to you, the investor, or to advisors in communicating with your clients. Any questions or feedback is always appreciated.

[i] Fidelity Investments. (2017). “Fidelity Q3 Retirement Analysis: Average 401(k) and IRA Balances Climb 10 Percent Over The Last Year, Continue To Hit Record Levels”. Retrieved from Fidelity.com

[ii] Social Security Administration (2017). “Benefits Planner: Income Taxes And Your Social Security Benefits”. Retrieved from ssa.gov

Disclosure: I am/we are long VTI, VXUS, VCSH, VCIT, VMBS, VFIIX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Peak Capital Research & Management’s clients are long the following positions in either Vanguard ETFs or Mutual Funds or utilizing a similar iShares ETF. Broad US Index, Broad International Index, short-term corporate bonds, intermediate-term corporate bonds, and GNMAs.