Looking for consistent distribution hikes and consistent growth? You may want to take a look at Holly Energy Partners L.P. (HEP), whose management has achieved quite a long string of distribution hikes and impressive CAGR since the company’s IPO.

Profile:

HEP is a Delaware LP formed in early 2004 by HollyFrontier (HFC) and is headquartered in Dallas, Texas. HEP provides petroleum product and crude oil transportation, terminalling, storage, and throughput services to the petroleum industry, including HollyFrontier Corporation subsidiaries.

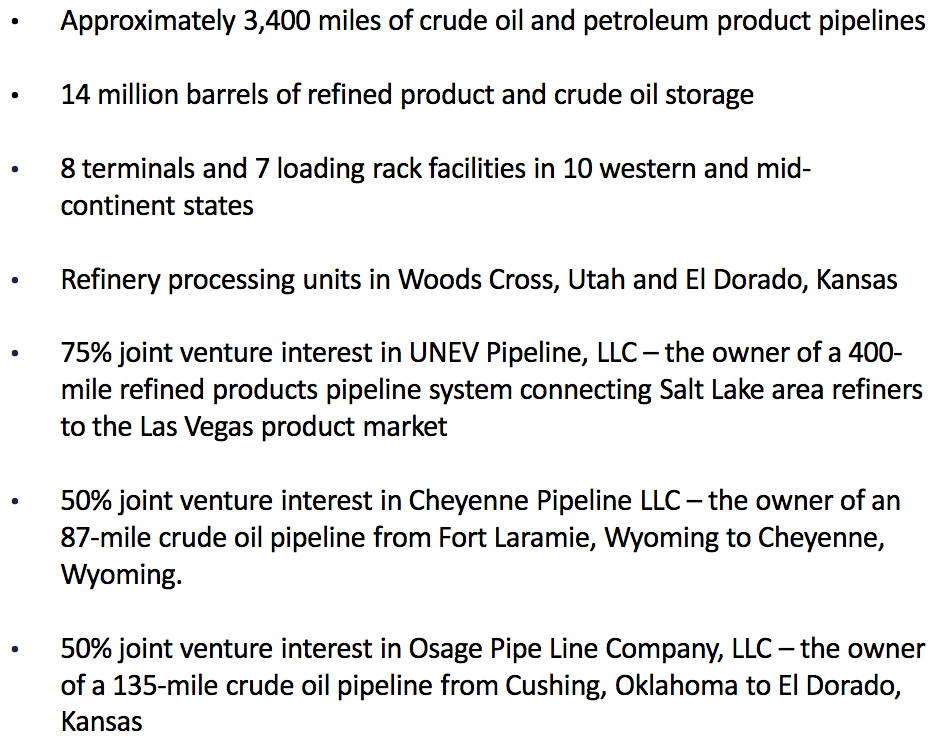

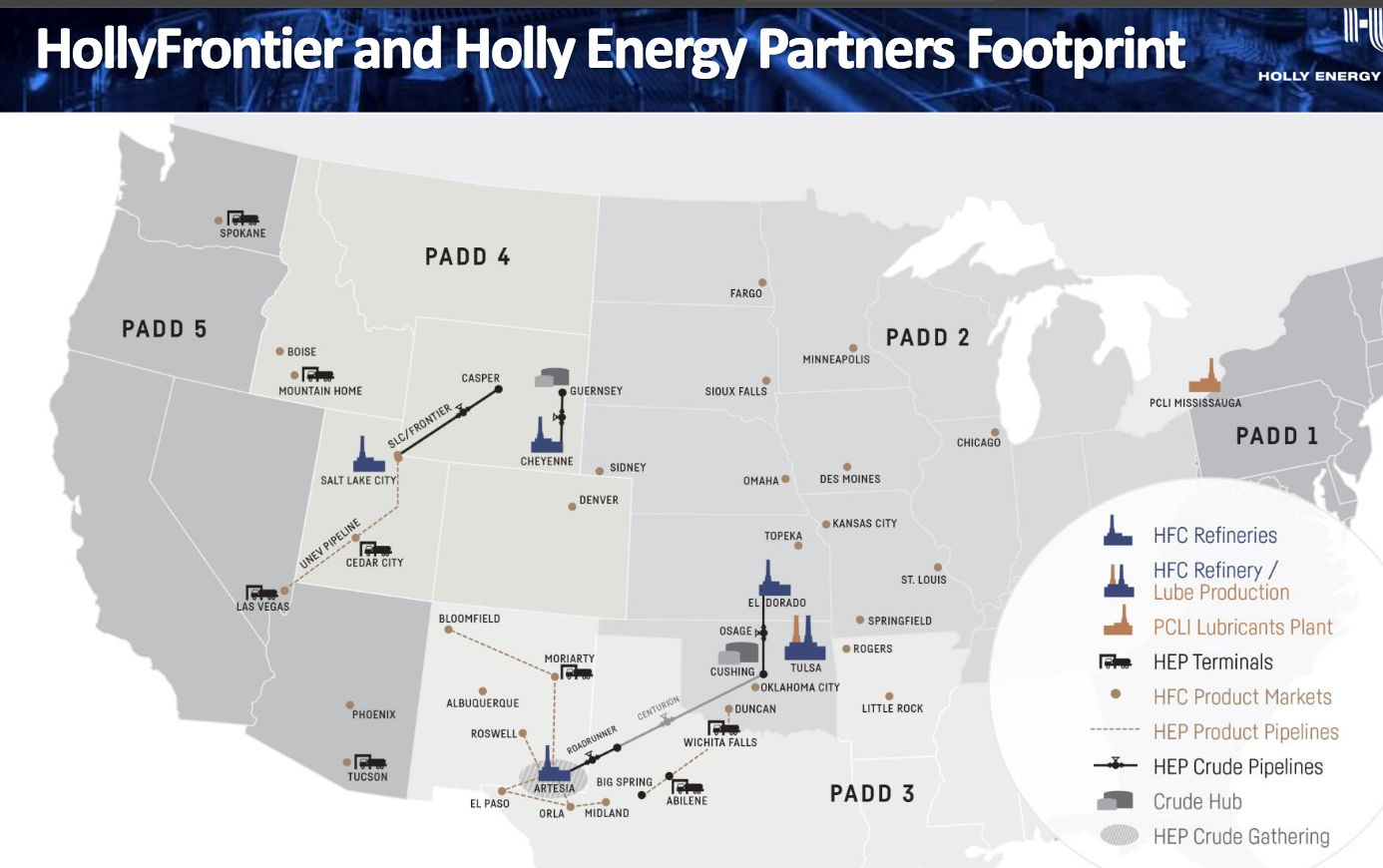

HEP’s assets include:

(Source: HEP site)

(Source: HEP site)

Distributions:

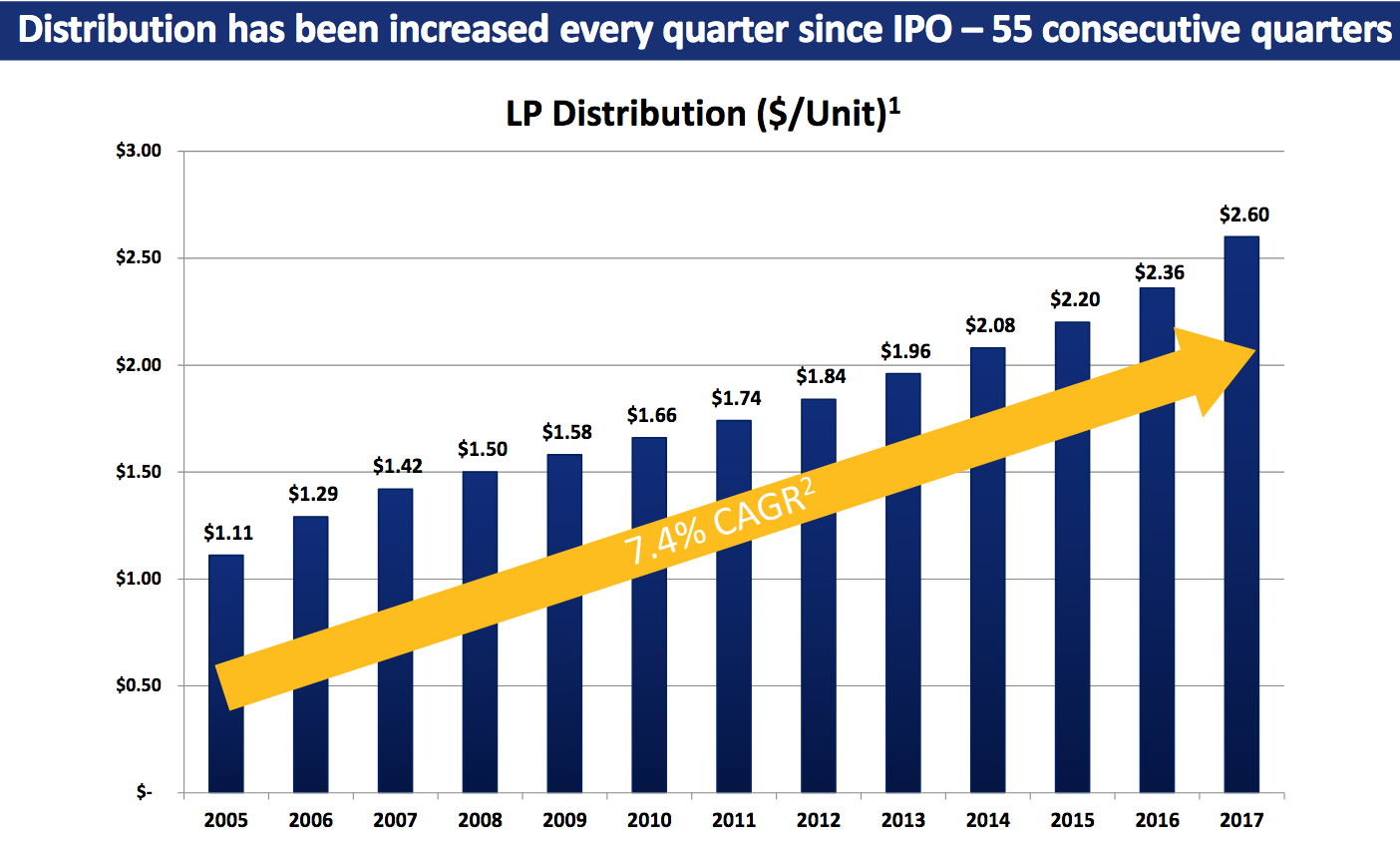

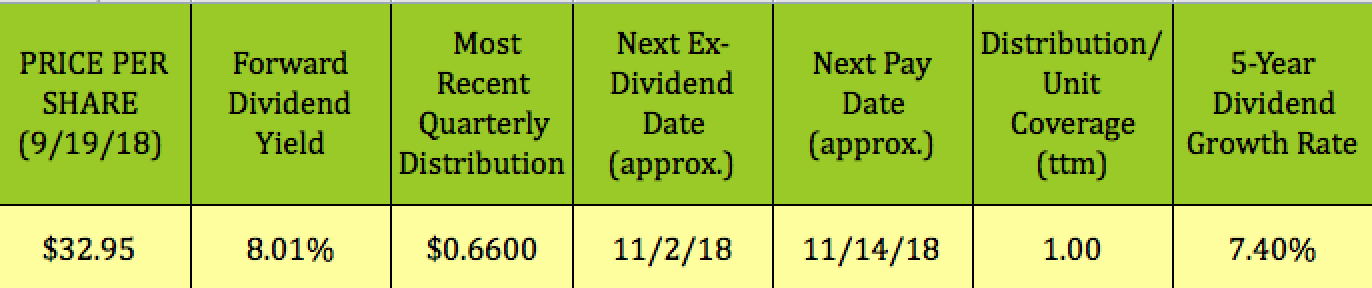

Management has raised the quarterly distribution for 55 straight quarters, delivering a 7.4% CAGR since HEP’s IPO.

(Source: HEP site)

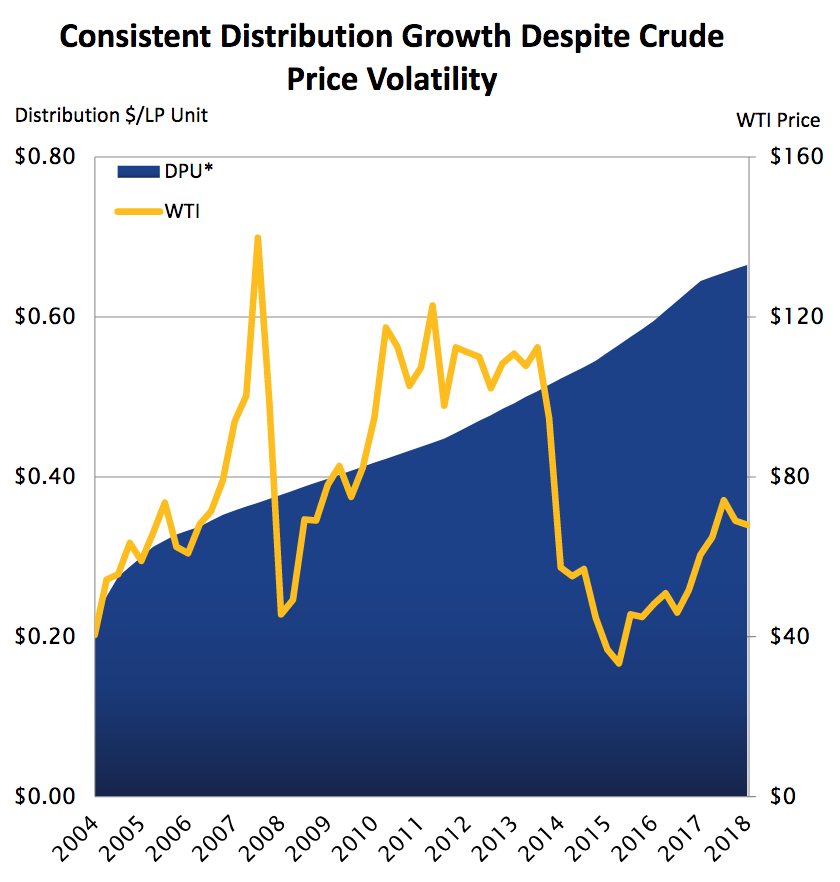

One of HEP’s strengths is that it has been able to keep raising its distributions through various boom and bust cycles. The most recent downturn, in 2014 – early 2016, saw many LPs cutting or eliminating their payouts in order to stay afloat. HEP’s management, however, kept the payout party going right through the downturn.

HEP pays in the usual Feb./May/Aug./Nov. cycle for LPs and its unitholders get a K-1 at tax time. Its next payout should go ex-dividend ~11/2/18. Given its past quarterly hike increments, the November payout will probably bring the distribution to ~$0.665/unit.

(Source: HEP site)

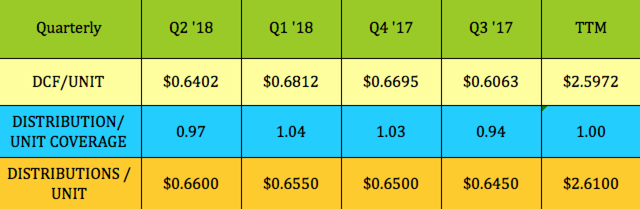

Although the quarterly hikes have been consistent, HEP’s distribution coverage has been less than robust over the past four quarters, running between ~.94X in Q3 ’17 and 1.04X in Q1 ’18.

There’s some seasonality with HEP’s operations, particularly its joint venture UNEV pipeline, as management pointed out on the Q2 ’18 earnings call:

Coverage was adversely effected by typical seasonal factors on UNEV, while we expect a significant improvement in the second half of 2018 to the contractual tariff escalators effective on July 1. We continue to expect our coverage ratio to be 1 times or higher for the full year 2018.”

Options:

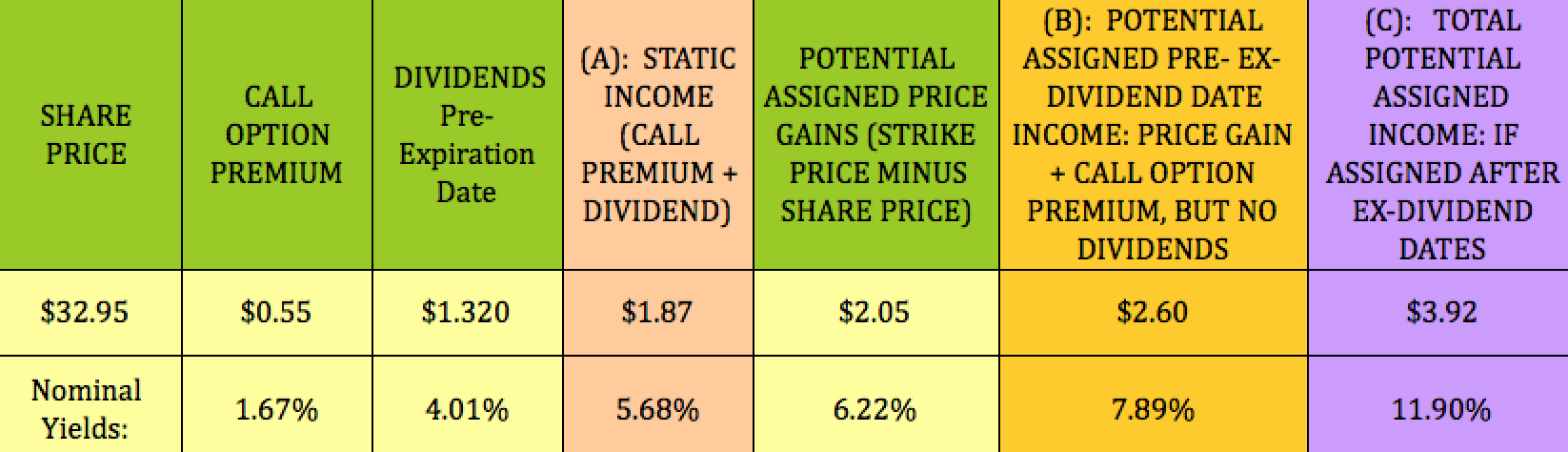

If you’re more interested in a relatively short-term trade, here’s a February 2019 covered call trade which we just added to our free Covered Calls Table. The February $35.00 call strike has a bid of $.55, a bid less than HEP’s most recent $.66 payout.

These are the three main profitable scenarios for this trade – static, assigned before the ex-dividend date, and assigned after the second ex-dividend date. $2.05 leaves quite a bit of headroom between HEP’s $32.95 price and the $35.00 strike, giving ample coverage if HEP’s price/unit should rise and the units were to be assigned prior to the ex-dividend date.

We’ve added this February trade for HEP to our free Cash Secured Puts Table, where you can find more details for it and over 30 other trades.

If you’re leery of buying HEP at its current price level, the February $30.00 put strike pays $.90 and gives you a breakeven of $29.10.

Earnings:

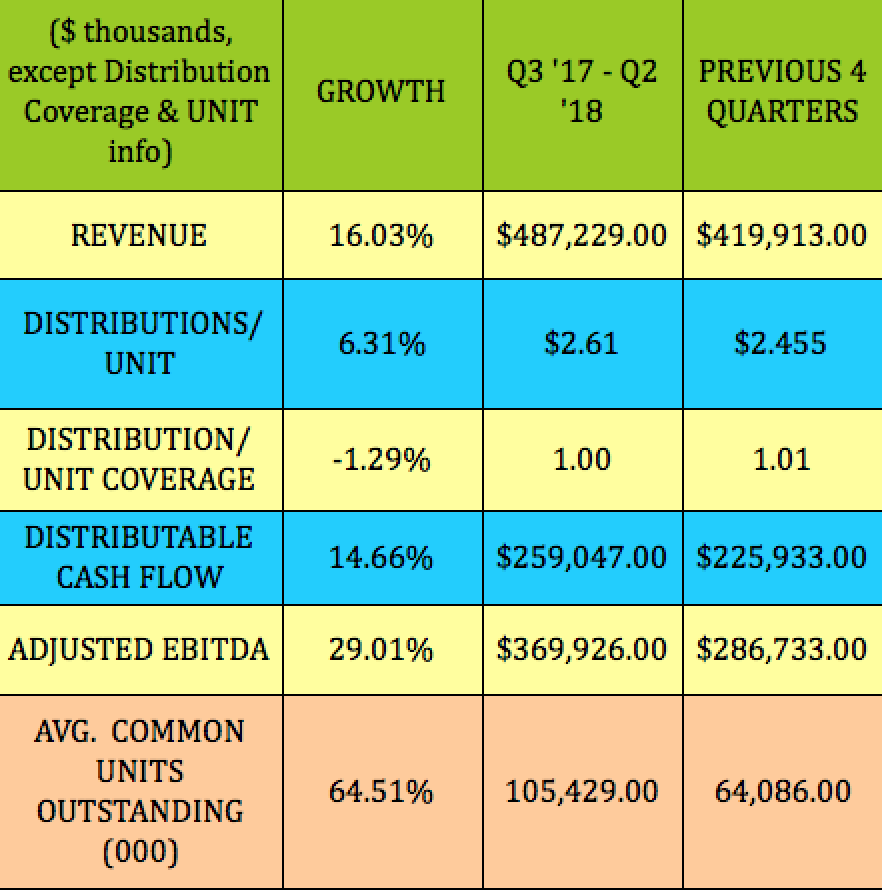

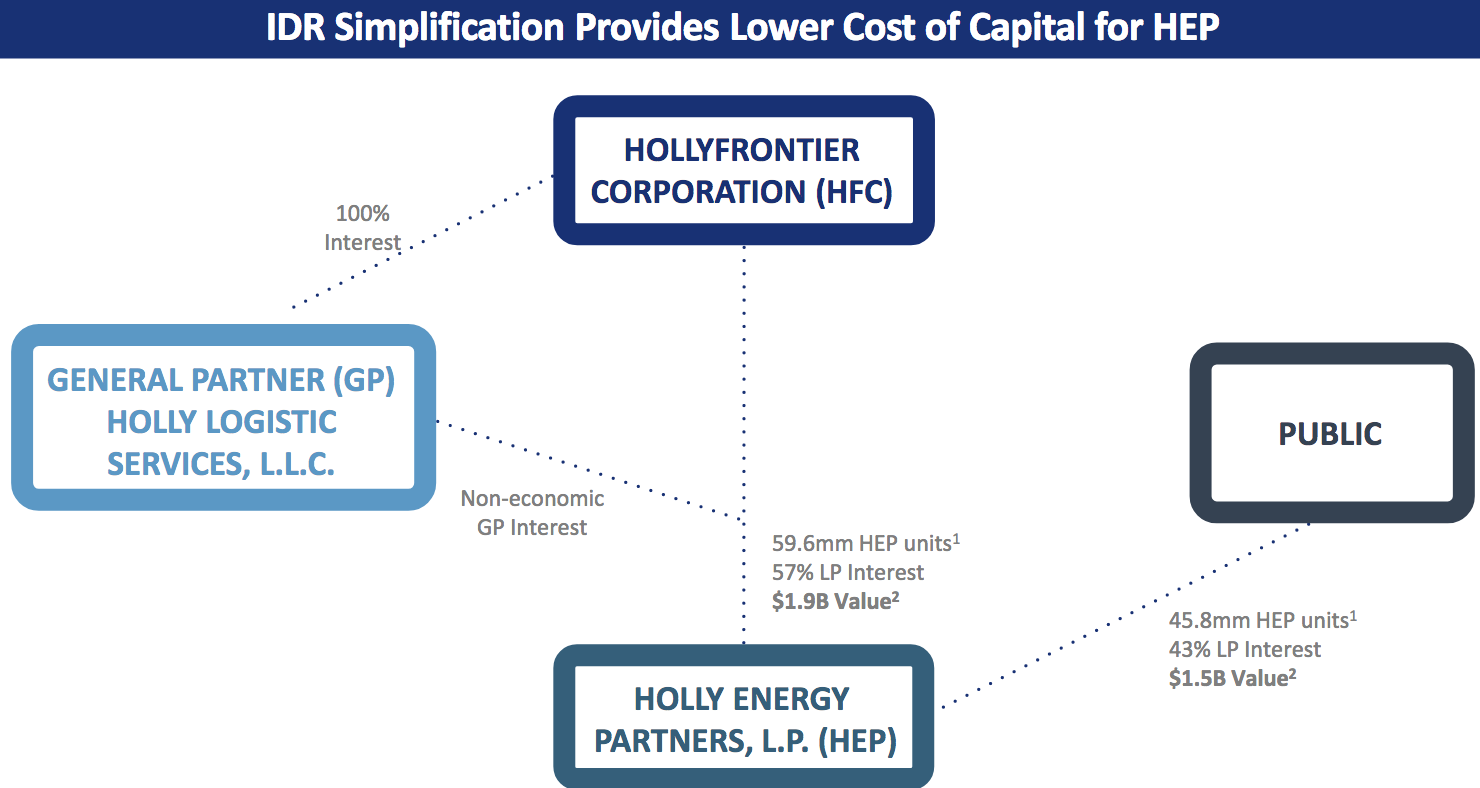

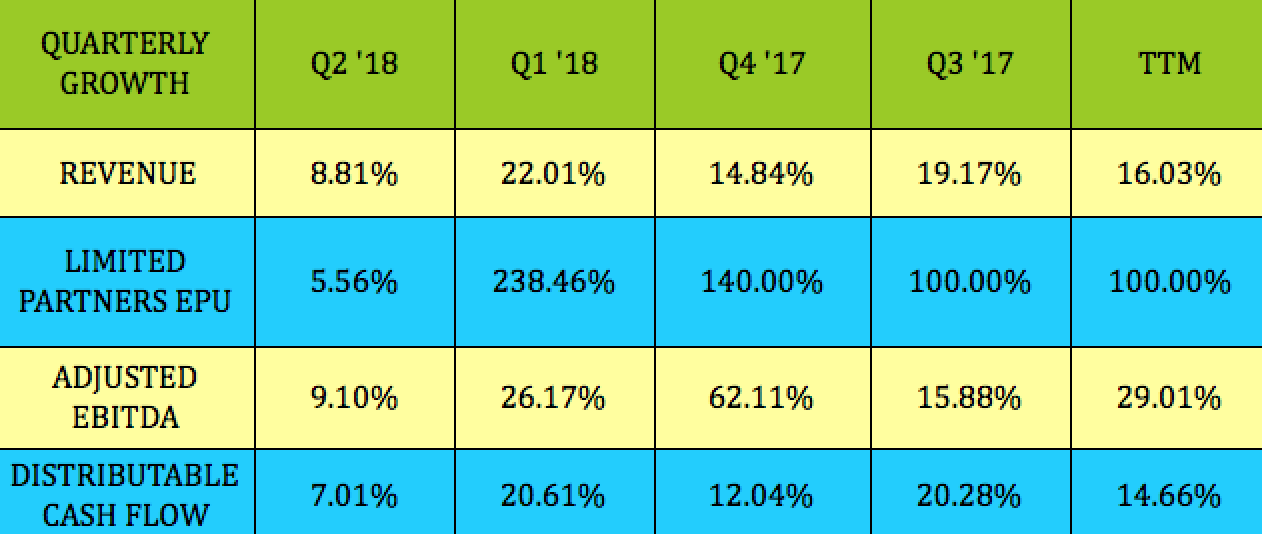

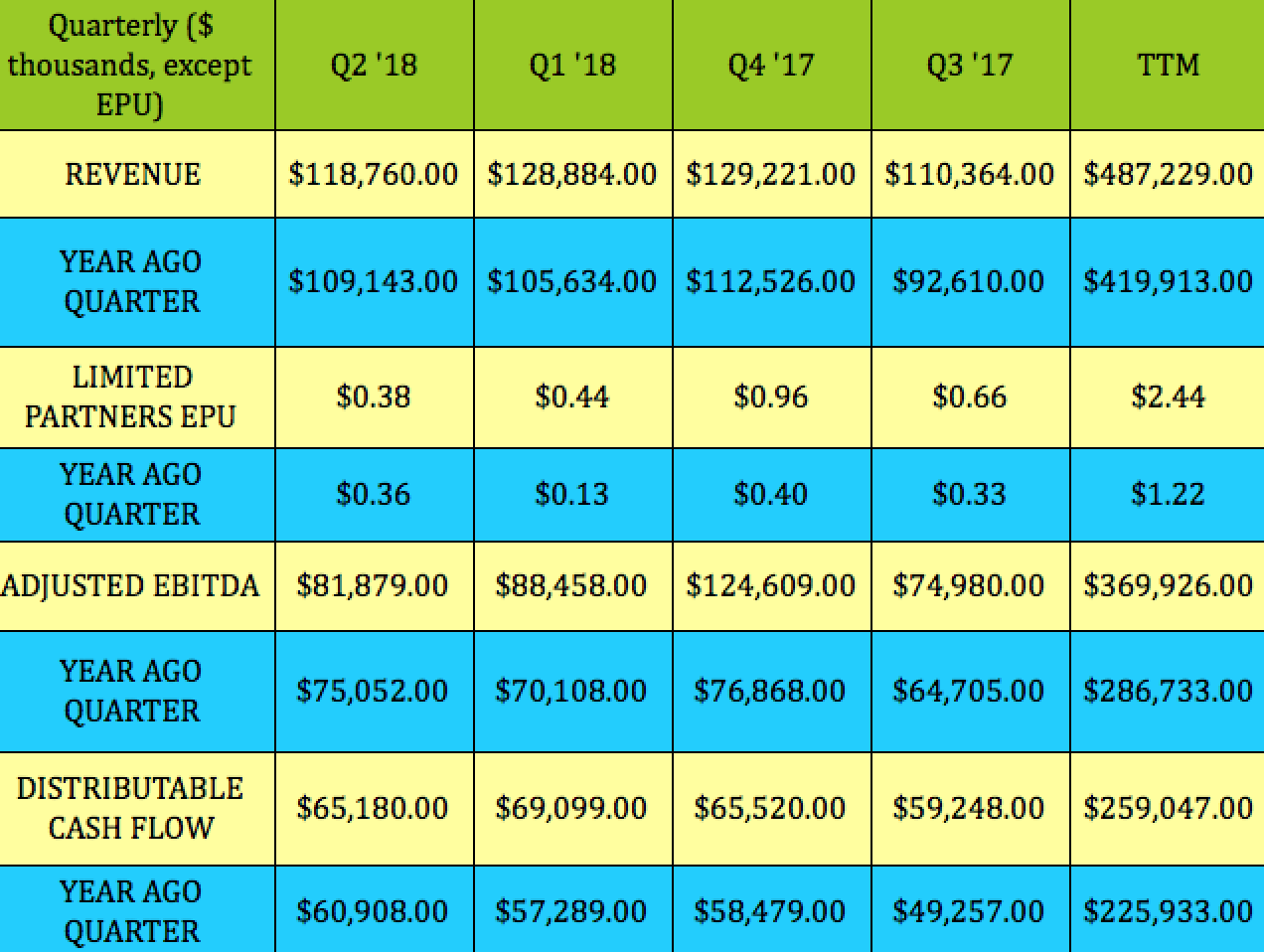

HEP’s coverage also was ~1X in the previous four quarters, running from .93X to 1.07X. Although EBITDA rose 29% and DCF rose 14.7% in the most recent four quarters, HEP’s unit count rose by 64.5% due to the big IDR swap deal that HEP did with HFC in October ’17.

That deal eliminated the incentive distribution rights held by HEP’s GP and converted HEP GP’s 2% general partner interest in Holly Energy into a non-economic interest in exchange for the issuance by Holly Energy of 37,250,000 of its common units to HEP GP.

(Source: HEP site)

Year-over-year, HEP has had good growth over the past four quarters due to its acquisition of the remaining interests in the SLC and Frontier pipelines in late 2017.

Sequentially, it looks like HEP’s earnings peaked back in Q4 ’17, but that quarter’s EBITDA and net income were pumped up by a $36.3M one-time gain related to the re-measurement to acquisition date of the fair value of HEP’s preexisting equity interests of the SLC and Frontier pipelines. Without that one-time gain, EBITDA would’ve been ~$88M, very similar to HEP’s Q1 ’18 EBITDA figure.

As we mentioned earlier, Q2 ’18 had some seasonal headwinds for HEP, which produced lower earnings than Q1 ’18.

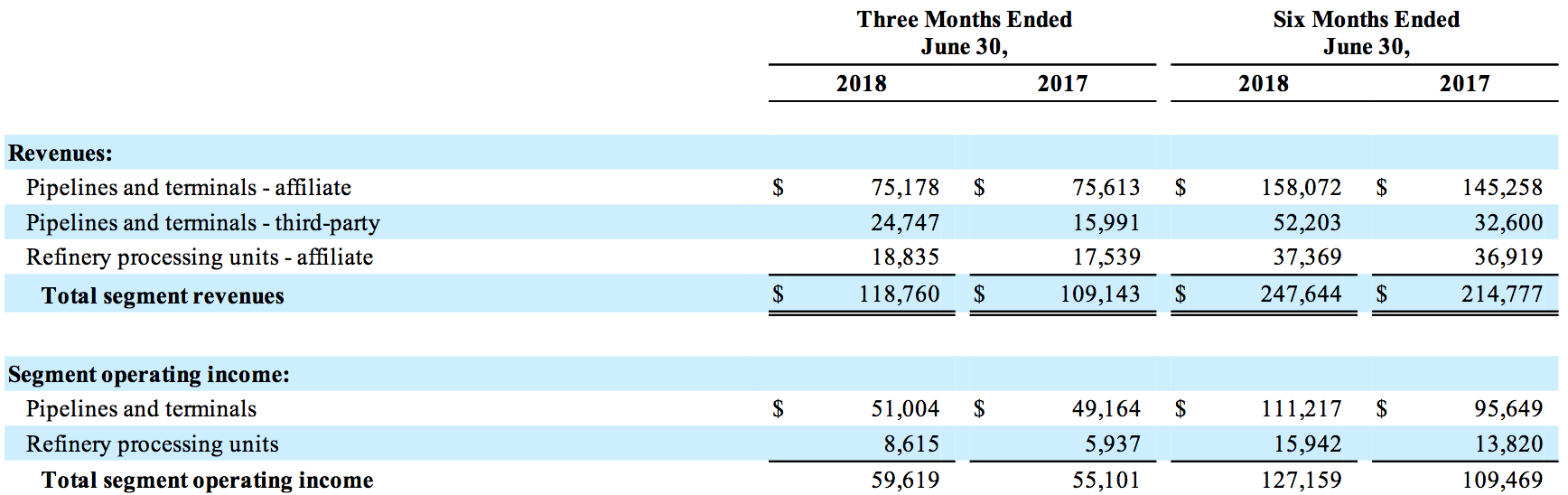

Segments:

Segment revenue has risen by 15.3% so far in 2018, with the biggest gain coming from third-party pipelines and terminals, which rose by 60%. Pipelines and terminals contributed 87% of operating income in Q1-Q2 ’18, which was up by ~16%.

(Source: Q2 ’18 10-Q)

Risks:

Dilution – The IDR deal has been somewhat dilutive to the distribution coverage in 2018. However, management is still targeting full-year 2018 distribution coverage of 1X, with higher coverage ratios in the second half of the year due to contractual tariff escalators.

Debt – In a capital-intensive industry, such as energy infrastructure, debt is often the gorilla in the room. Fortunately, HEP’s management has been able to reduce its net debt/EBITDA leverage to 3.75X, as of Q2 ’18 vs. 4.26X in Q2 ’17. (More on this in the Financials section.)

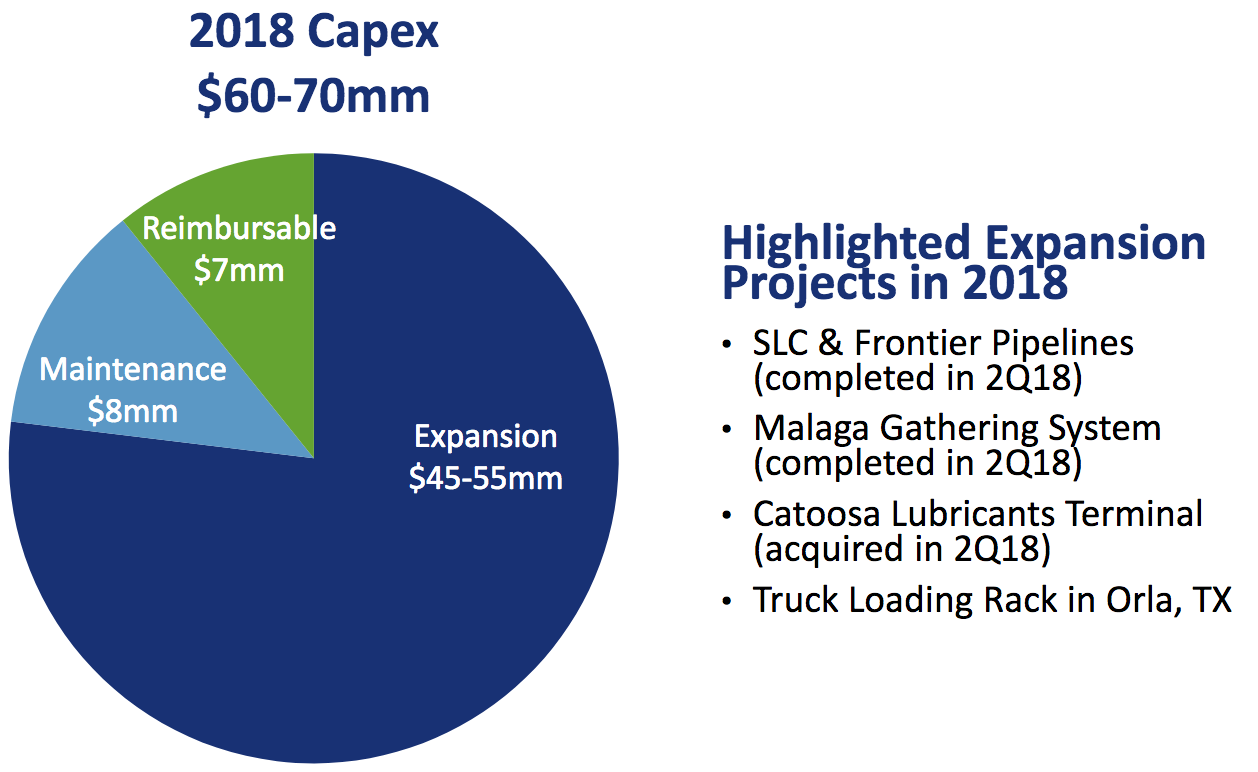

Growth Projects:

As we look toward the second half of 2018, HEP plans to continue expanding our logistics infrastructure to serve the growing distillate demand in the Permian Basin. In May, we announced our intention to construct a new truck loading rack in Orla, Texas. This facility will be able to deliver up to 30,000 barrels per day of diesel that would otherwise be rail or tuck into the area. Construction is underway, so we expect this rack to be operational by the end of the year.” (Source: Q2 ’18 call)

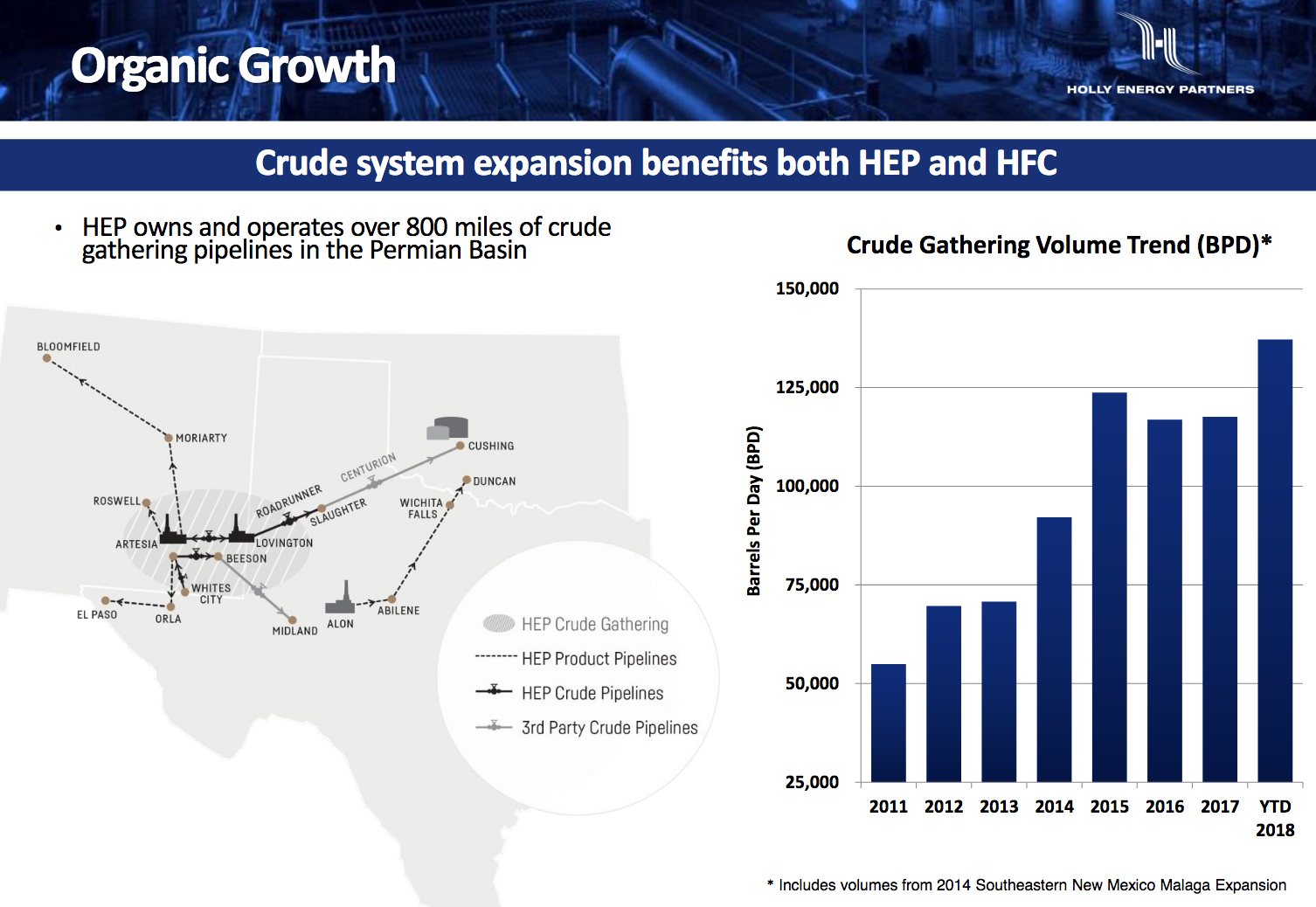

HEP’s crude gathering volume trended lower in 2016 vs. 2015 and was ~flat in 2017. However, 2018 barrels/day volume has set company records, surpassing 2015’s volume.

(Source: HEP site)

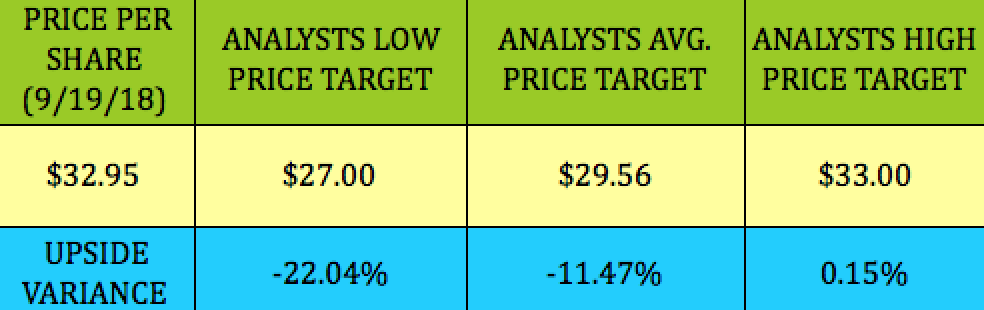

Analysts’ Price Targets:

At $32.95, HEP is 11.5% above analysts’ average price target of $29.56 and is just about even with the $33.00 high price target.

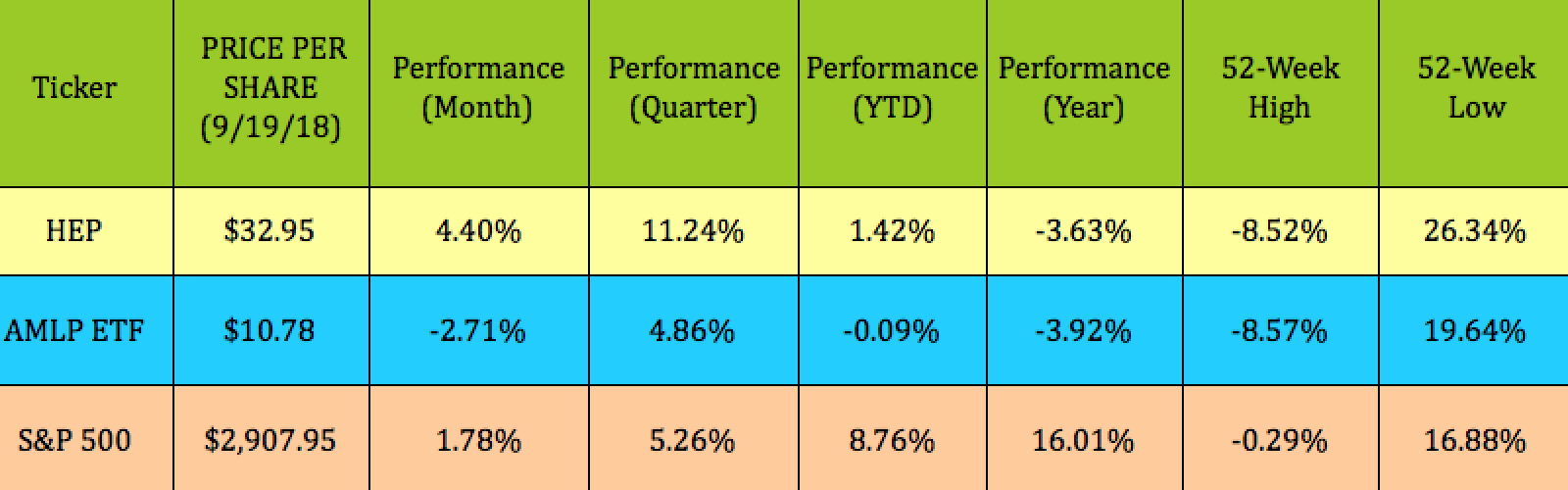

Performance:

Although HEP has outperformed the benchmark Alerian MLP ETF (AMLP) in 2018, it trails the broader market. However, it has caught a bid over the past quarter and has outperformed the S&P 500, rising 11.24%.

Valuations:

Investors are giving HEP units a premium valuation over other midstream high yield companies. Those relentless quarterly hikes have created a lot of goodwill for HEP in the market, leading to higher P/book, P/DCF, P/sales, and EV/EBITDA, even with HEP’s lower distribution coverage and yield.

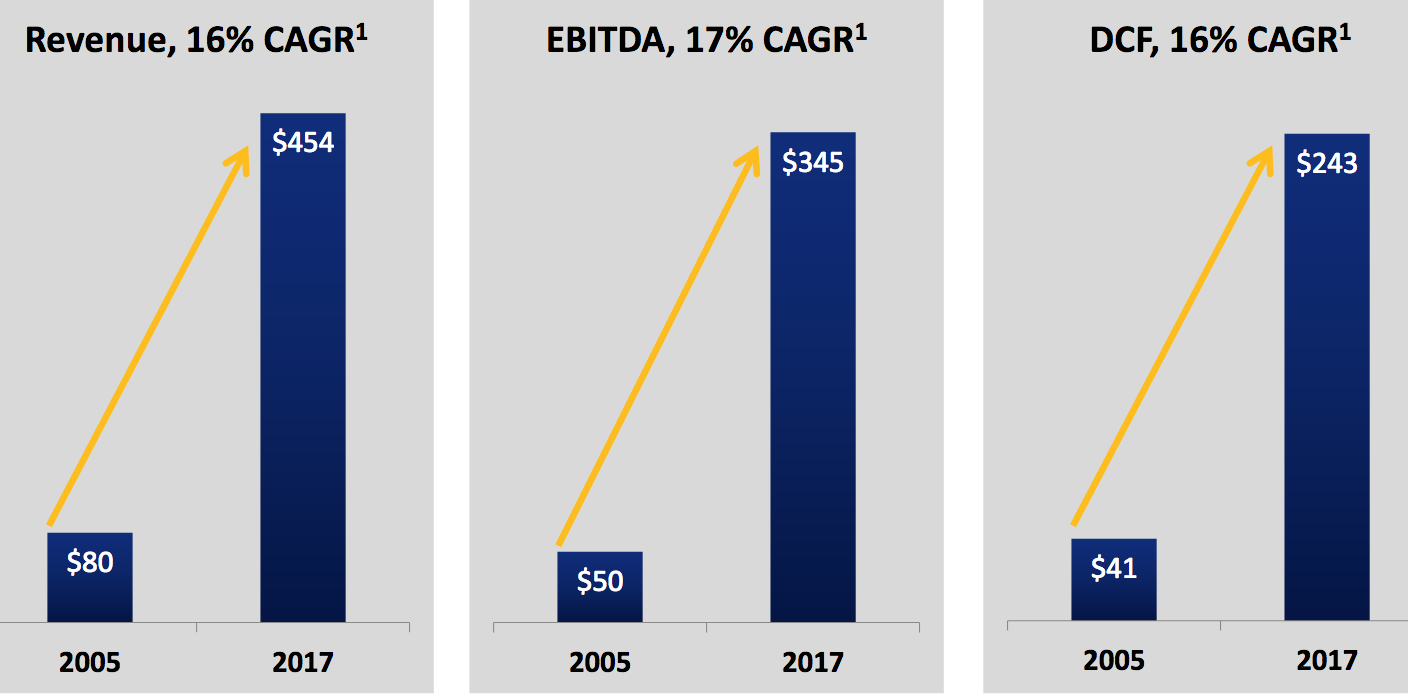

Another factor that has created a strong following for HEP is its long-term track record – management has delivered strong revenue, EBITDA, and DCF growth for unitholders since the IPO:

(Source: HEP site)

Financials:

We show HEP’s trailing net debt/adjusted EBITDA to be at 3.75 vs. management’s figure of 4.2X for net debt/EBITDA, due to higher adjusted EBITDA of $369.93M and net debt of $1388.94M. Management expects EBITDA leverage to be around 4X by the end of 2018, which would be roughly in line with other high-yield midstream companies we cover.

Total debt/equity has inched down to 2.98X since Q2 ’17, as have HEP’s ROA, ROE, current ratio, and operating margin. Compared to other high-yield midstream companies we cover, HEP has a much better ROE and operating margin.

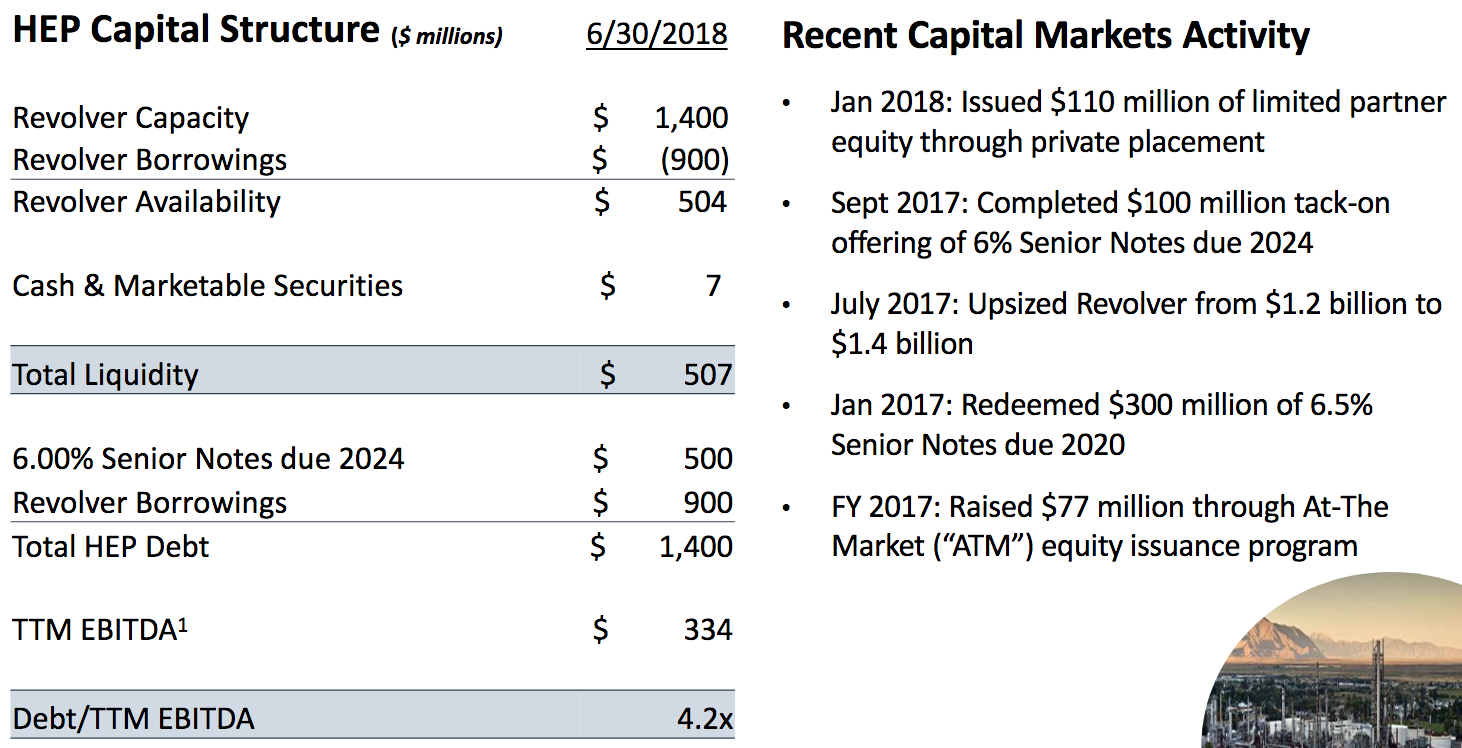

Debt and Liquidity:

HEP has a $1.4B senior secured revolving credit facility expiring in July 2022 and $500M in Senior Notes, which expire in 2024. As of 6/30/18, its current liquidity was ~$507M.

(Source: HEP site)

HEP also has a continuous offering program under which they may issue and sell common units from time to time, representing limited partner interests, up to an aggregate gross sales amount of $200M. In Q1-Q2 ’18, HEP issued 17,1246 units under this program, providing ~ $5.2M in gross proceeds.

Summary:

This is one for the watch list. There’s a lot to like about HEP – we just don’t like the current price as an entry point. Long term, HEP’s management has a good track record in terms of ROE, DCF, EBITDA, and DCF growth.

However, its current price/unit of $32.95, which sits right near the high price target of $33.00, and its higher valuations vs. other high-yield midstream firms, give us pause. We rate HEP a Hold and intend to either wait for a pullback and/or perhaps sell cash secured puts below HEP’s price/unit, in order to get paid to wait and have a lower breakeven.

All tables furnished by DoubleDividendStocks.com unless otherwise noted.

Disclaimer: This article was written for informational purposes only and is not intended as personal investment advice. Please practice due diligence before investing in any investment vehicle mentioned in this article.

CLARIFICATION: We have two investing services. Our legacy service, DoubleDividendStocks.com, has focused on selling options on dividend stocks since 2009.

Our Marketplace service, Hidden Dividend Stocks Plus, focuses on undercovered, undervalued income vehicles, and special high yield situations.

We scour the US and world markets to find solid income opportunities with dividend yields ranging from 5% to 10%-plus, backed by strong earnings.

These stocks are often small cap, low beta equities that offer stronger price protection vs. market volatility.

We publish exclusive articles each week with investing ideas for the HDS+ site that you won’t see anywhere else.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: We may sell cash secured puts below HEP’s price/unit in the near future.